The Macro Code #7: An in-depth look at the long-term game between German economy and Chinese politics

German elections: not only fiscal policy. There is a trade policy challenge to face

Welcome to The Macro Code, an open diary on markets, macro-trends and structural changes.

German federal elections will take place on September 26, after nearly 16 years of Christian Democratic Union (CDU) rule under the leadership of Angela Merkel.

How much do elections matter for policies and markets?

This is a central question for markets and investors.

In a previous newsletter (available here: The Macro Code #3: Germany elections and the fiscal conundrum) we discussed how the September 26th elections will affect German fiscal policy and what the implications will be for the markets.

In this new edition of The Macro Code, we look at what impact the federal election will have on German trade policy.

The agenda can be split into three key points:

What structural weaknesses are plaguing Germany's competitiveness?

Does the export-led German model still work?

How can the long-term game between the German economy and Chinese politics be broken up?

Germany's competitiveness

Angela Merkel's political era is drawing to a close. During her four terms in office, the German Chancellor has dealt with some of the biggest political and financial crises of recent history with rigor and discipline (GFC, Sovereign Debt Crisis, Refugee Crisis, COVID-19). The Merkel era has repeatedly succeeded in saving the Eurozone from collapse by pulling the German economy out of each and every emergency under relatively strong conditions. However, in the area of more structural economic policies, the Merkel era has struggled to come up with a concrete result, showing how complicated visionary decision-making can be.

The German economy is one of the strongest within the Eurozone: the economy is close to full employment and public finances - before the pandemic - were in a very healthy state. But in recent years, many analysts have questioned the long-term viability of the German economic model. Why? Because as one of the world's leading exporting countries, the most important supply hub for Europe, a source of hidden champions, and a strong research and development base, Germany has struggled to capitalize on its domestic resources, and in the face of a changing trade landscape, German industry could lose its key role in global competition.

Since the 2017 elections, Germany's competitive position has begun to weaken, showing no signs of improvement over time.

Germany's success is based primarily on traditional industries. "Traditional" does not mean obsolete. But German corporations play a minor role in the New Economy. Technology giants, in particular, have emerged stronger from crises. And even in traditional segments, Germany has a very strong competitor in China.

Germany lags behind internationally when it comes to education, digitization, and venture capital. But allowing risky ideas is vital to future economic success because it fuels innovation and challenges long-standing companies and corporate structures, increasing that competitiveness in the long term.

The German export-oriented economic model

The German growth strategy, characterized by a high share of net exports in GDP and a high contribution to growth by net exports, has made the country highly dependent on the external sector and economic performance of the trading partners.

Particularly, this has become clear in 2008/09 when real GDP dropped by 5.6% and net exports shrank by 24.5% (IMF 2015; OECD 2015) in the course of the crisis (although this slowdown was not as apparent during the supply crisis due to Covid-19). The real depreciation, as measured by the CPI-based real effective exchange rate and relatively low ULC growth, hint to improved price competitiveness in the period 1999 to 2007, which is in line with the arguments raised by advocates of the German competitiveness miracle.

However, moderate wage growth and the positive private, and now public, sector balance are rather indicative of weak consumption demand and investment activity. This has resulted in modest import demand and which in turn has contributed to the accumulation of the German current account surplus.

The empirical research conducted by Heinze (2018), shows that German exports are predominantly determined by foreign income demand and have benefitted from growth dynamics of its trading partners in- and outside the EMU. Consequently, based on this evidence in a context of political change and renewed dynamics of global competition, the new face of Germany needs to address the changing face of global trade.

Indeed, in recent years, the export-oriented German economic model has not proven to be effective, as it has been caught between tough American protectionism and aggressive Chinese industrial policy. As previously reported, this is a model that is centered on large trade and current account surpluses, which have not changed in the last decade.

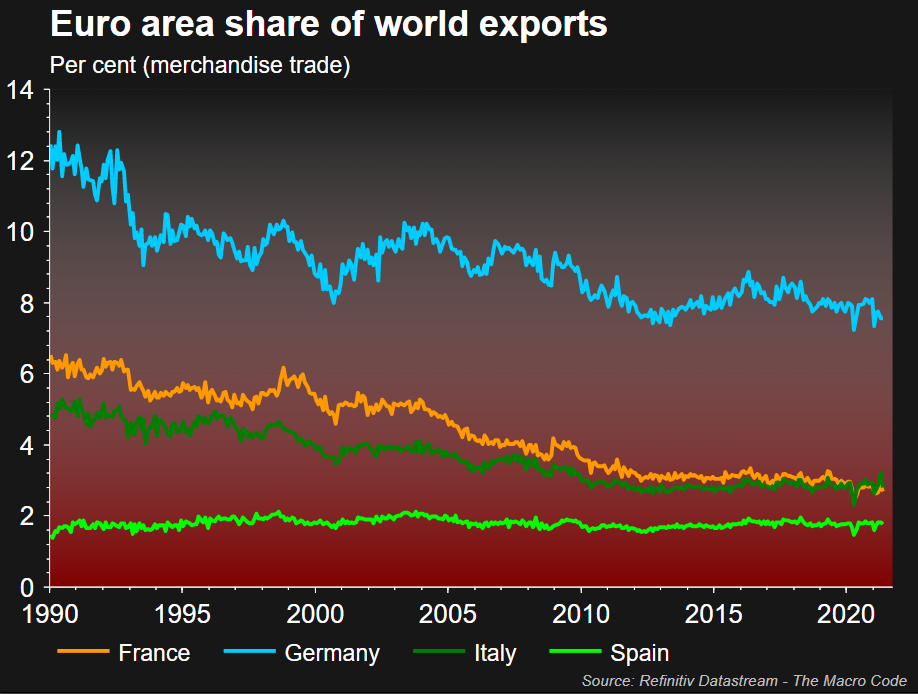

A look at the data shows that, compared to its 1990 peak, Germany's share of world exports has fallen by four percentage points. Exports of goods have tripled since 1990 as have imports.

As of today, about one in four jobs in Germany is dependent on exports. Measured as a percentage of GDP, exports of goods and services reached an all-time high of 47.3% in 2018, falling slightly to 44% in 2020. At the beginning of the millennium, this share was only 30.8%, growing almost without interruption until last year, while other countries experienced a stabilization or even a reversal of the trend.

What are the dangers of an export-led economic model?

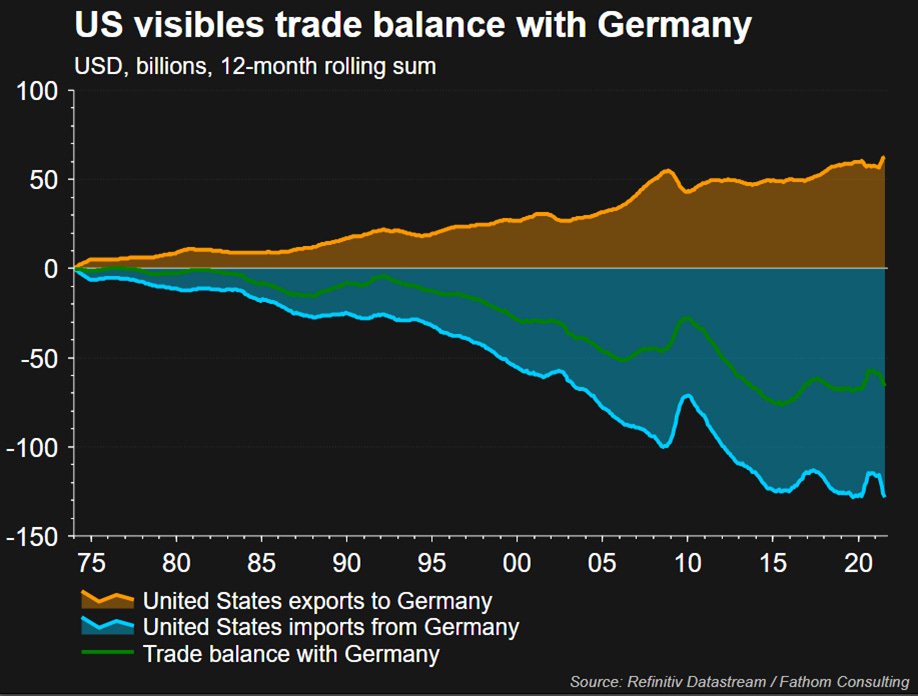

The trade tensions of recent years coming from the US (which started with a tough stance by Trump and continued with more moderate tones under President Biden) quickly generated a threat of imposing painful sanctions on major German export goods such as cars. Meanwhile, China's industrial policy has begun to target the acquisition of important industrial technologies and, in the medium term, to replace existing foreign technology leaders in the automotive, engineering, and chemical sectors.

As a result, due to the size of their markets, the U.S. and China undoubtedly have the tools to damage the export-oriented German economy. For this reason, Berlin should push for a more ambitious national and European innovation policy as well as a resilient European foreign trade policy.

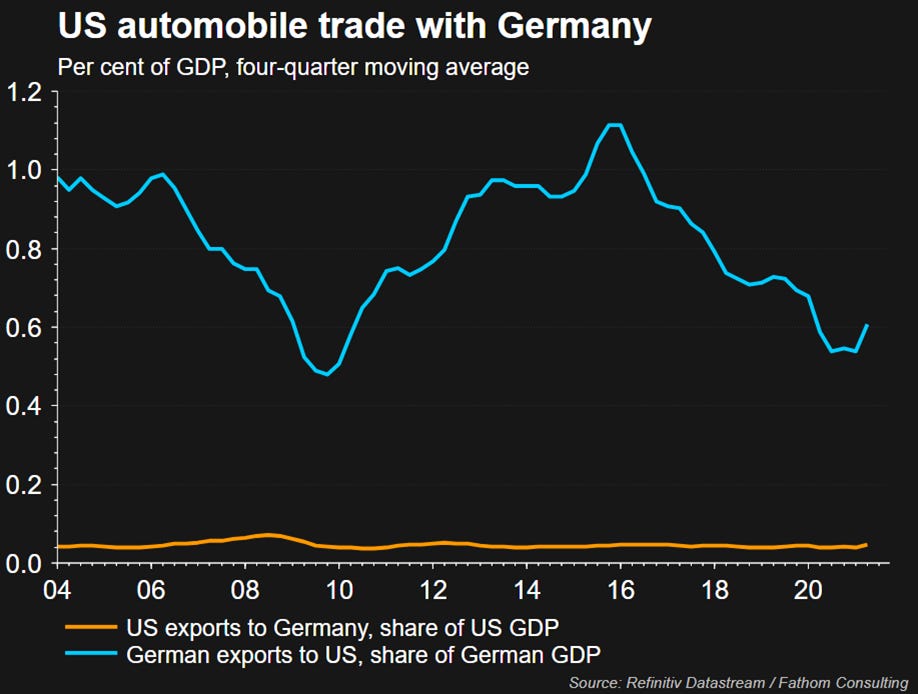

In addition, as detailed in the previous section, the German export success story is based on traditional sectors. Germany ranks first in the global export of automotive products, chemicals, and pharmaceuticals. In particular, the automotive sector will face complications related to new climate regulations.

This is why, as the automotive sector is by far the most important branch of industry in Germany in terms of turnover, a transition will soon be needed to ensure its growth and employment contribution.

Of course, this is not to argue that traditional sectors should take a back seat to innovative sectors. For example, the pandemic has shown that traditional sectors can quickly transform into new future markets, as is the case with pharmaceuticals. (It is estimated that the biotech company BioNTech - thanks to contracts related to the production of Covid-19 vaccine - could single-handedly lift the German economy by 0.5% in 2021.)

Ultimately, in light of trade tensions, emerging economies such as China setting national agendas to transform themselves into a manufacturing leader and high-tech powerhouse by 2025, the World Trade Organization progressively losing autonomy over compliance with market opening rules in key economies, and a global supply chain rethink resulting from the COVID-19 crisis that has pushed organizations to rethink just-in-time sourcing and manufacturing by shortening supply chains (as outlined well in this Capgemini report), Germany will need to rethink its trade policy. The German economy will need to be able to unleash internal growth forces.

This is compounded by the fact that the largest share of German exports is made by SMEs and not by German multinationals. In fact, companies operating in product niches, the so-called Mittelstand, and its hidden champions, are largely unknown to the public and have a turnover of less than five billion euros, but have been an important factor in Germany's export success for decades. Contrary to estimates, more than 1,500 companies in Germany rank among the hidden champions, half of all estimated companies worldwide. A list of hidden champions conducted in 2019 through 2016 shows that most companies are active in manufacturing with a specific focus on machinery, followed by electronics and optical products.

But the competition is coming...

How can the long-term game between the German economy and Chinese politics be broken up?

According to a study by Merics, Germany has created dependencies on China in about 100 commodity categories since 1978.

Within the EU, Germany has benefited most economically from China's rise.

Deeper political ties under the leadership of Chancellor Angela Merkel have flanked stronger trade and investment relationships since 2005. Germany accounts for 48.5% of EU exports to China, 4.6 times more than France, the bloc's second-largest exporter to China by value in 2019. In the second quarter of 2020, China became Germany's largest export market for the first time as other major markets, including EU members and the United States, continued to suffer from the Covid-19 pandemic. Germany's flourishing economic relationship with China remains an exception within the EU.

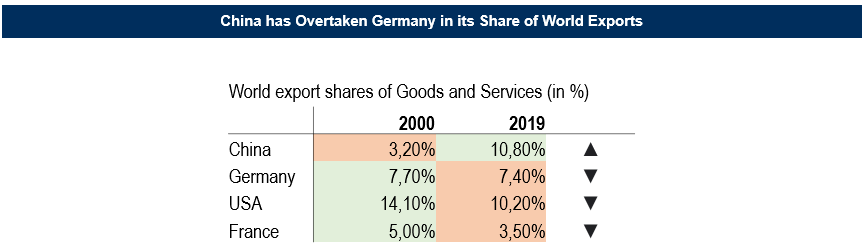

While China has overtaken Germany in export production, it is in Germany's interest to diversify and explore new markets and production sites to avoid worsening dependencies.

Closer scrutiny and better risk management, as well as targeted technology controls, are needed, as Germany has long failed to protect its technology and knowledge flow in China.

In 2015, Beijing released its "Made in China 2025" plan to replace Germany as a producer of quality goods.

The plan aims to achieve independence from foreign suppliers, the initiative encourages increased production of high-tech products and services, aiming for China to dominate in ten key sectors, including electric cars, IT, aerospace, machine building of different types and medical technology.

German diversification away from its growing dependence on China will not and cannot be rapid, but it needs to begin immediately. It requires political leadership and should focus on allies. Overall, it is important to remember that only 8% of German exports go to China while 67% go to Europe.

China is using micro-policies and regulations to resolve the many rifts that have accumulated over the past few decades, with the goal of no longer being strictly dependent on advanced economies, but rather to become a supplier - producer - originator and cover supply chains across the board.

A country with an export-oriented economic model like Germany needs to look more at its long-term prosperity. This is especially valid given China's new economic strategy of "dual circulation", a form of import substitution and further decoupling that is increasing pressure on German companies to locate in China, transfer more intellectual property, and transfer research and development (President Xi Jinping in May 2020 said that China will rely primarily on "internal circulation" - the domestic cycle of production, distribution, and consumption - for its development, supported by innovation and economic improvement).

Once the new German government is in place, it should act quickly to initiate a national security review of where China is going and what it means for Germany, politically and economically.

Key takeaways

On the trade policy front, the new German government and the Bundestag should pay attention to a few key issues:

1) Diversify away from China by examining Germany's foreign trade and tax policies, thereby creating preferential conditions for investment outside of China.

2) Germany should become much better at commercializing the technologies it develops instead of allowing them to be transferred elsewhere, thereby losing control of both the technologies themselves and market share. It needs to learn to invest internally. (This means incentivizing investment in risk capital and actively promoting a Capital Market Union agenda).

3) Security interests in foreign investments and acquisitions need to be properly examined, and a pan-European coordination office needs to be set up to protect strategic technologies from acquisition through market manipulation practices.

4) The rethinking of fiscal policy (polls predict an upward trend for the leftist coalition, and this would bring about a break with the fiscal conservatism represented by the deficit policy of the "Schwarze Null" and the constitutional limit on debt) will have to travel on the same channel as trade policy.

The Macro Code is an open diary on markets, macro-trends and structural changes.

To receive updates in newsletter format, follow the form below.

Please, note that The Macro Code represents personal views only.