The Macro Code #3: Germany elections and the fiscal conundrum

Towards a more flexible German fiscal policy? Beyond the debt brake.

Welcome to The Macro Code, an open diary on markets, macro-trends and structural changes.

The question is not whether we are able to change but whether we are changing fast enough.

Angela Merkel

The German federal election on September 26 will determine who will succeed Angela Merkel after her 16 years as chancellor. Without mincing words, the implications for Europe could be significant and long-lasting. Why? Essentially, because in a post-pandemic recovery environment, Germany has a critical responsibility to advance profound reforms.

The goal of this newsletter is to understand what will come after the Merkel era.

We will start with a review of the current political scene, then we move to macro considerations to take a closer look at the German economic landscape with the aim of understanding how the elections will affect Germany's fiscal policy and what the implications will be for the markets.

The political framework: the game's in play

After multiple distractions (the vaccine race, the devastating July flood, the geopolitical turmoil of Afghanistan) the chancery rush finally seems to have come full circle.

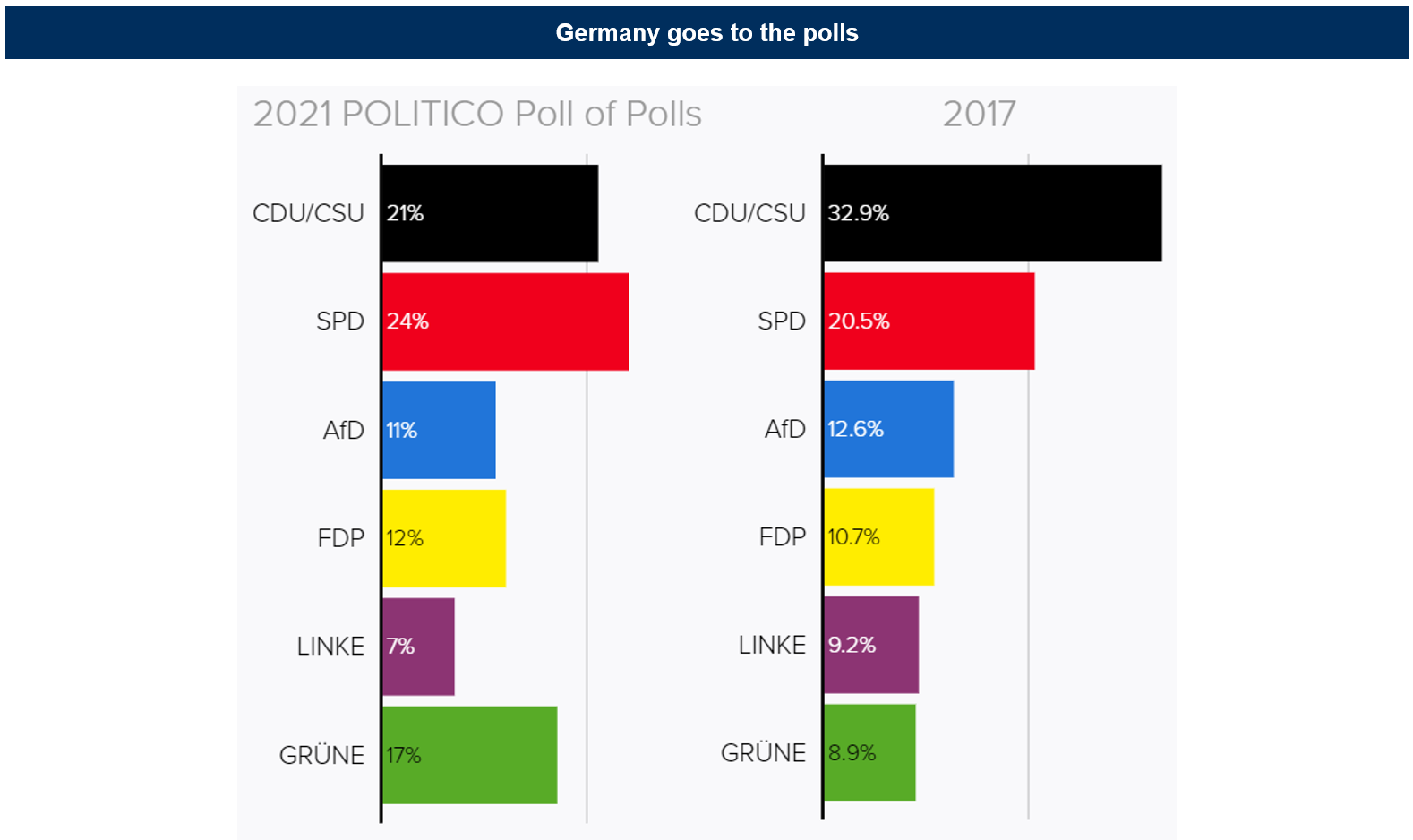

On Sunday, August 29, the first television face-off was held between the three main candidates: Armin Laschet for the Christian Democrats (CDU-CSU), Olaf Scholz for the Social Democrats (SPD) and Annalena Baerbock for the Greens (Grünen). According to an initial poll, the televised confrontation was won by Scholz, followed by Baerbock and then by Laschet. On the other hand, for some time now Scholz has been indicated as the preferred candidate for the chancellery by over 30% of Germans, thus far outstripping Baerbock (15%) and above all Laschet (11%). A few days ago it was reported that the Socialist Party reached 23% in the polls, thus overtaking the Christian Democrats for the first time in 15 years. A result that, if confirmed by the polls, would give a certain luster to the SPD that only a few months ago seemed to be in free fall. On closer inspection, however, with 23-24% of the vote, the Socialists would “only” garner 3% more votes than their historic low in the previous federal elections.

Looking at things from a different perspective, the big news is not about the good socialist performance, but rather the bad performance of the post-Merkel CDU/CSU that with 22% of the vote would lose 10% compared to the previous election.

What government can we expect from the upcoming elections and what domestic and international policies might be implemented?

In the 16 years with Angela Merkel, the Grosse Koalition between the CDU/CSU and the SPD has been repeated three times out of four, the only exception being the second Merkel government (2009-2013) when the Christian Democrats went into government with the liberals of the FDP. Germany's "broad understandings" have been a game of two, yet this does not seem a likely scenario for the next government. In fact, for the first time, we may find ourselves forced into a three-way coalition. If indeed the Socialists come in first, the Christian Democrats - who have been in government for 50 of the last 70 years - could be left out of the executive.

Only a few weeks ago, the CDU-CSU coalition with the Greens seemed the most likely, perhaps with the insertion of the liberal 'yellows' in what is called a "Jamaica" coalition. With the overtaking of the Socialists, however, a further scenario could develop in which Scholz's Socialists go into government with the "traffic light" coalition, therefore with the Greens and the Liberals. The more extreme left of Linke as well as the extreme right of Alternative für Deutschland (AfD) would remain outside the government.

What can we expect from a three-way coalition? First, a rather long time for the formation of the government. In fact, Germans tend to set government priorities in a prior agreement (Angela Merkel had to negotiate for 171 days with the Socialists in the last government). Second, in a three-party government, the negotiation could be even more complex and exhausting, also because the distances between the parties appear to be considerable both on domestic policies and on European and international ones.

The German economic context

The main German parties have different ideas, in some cases very divergent, especially in the fiscal, monetary and macroeconomic areas. In an unprecedented three-way coalition, it will be necessary to seek a synthesis, but this could threaten the stability of the government especially in the absence of a strong chancellor.

Let's take a brief look at Germany's economy.

The German economy has been gradually recovering from the output drop it suffered in 2020. GDP rose by 1.5% in Q2 (quarter-on-quarter), having declined at a similar pace in Q1. Gross domestic product grew an adjusted 1.6% on the quarter, up from its previous estimate of 1.5% and following a revised first quarter contraction of 2%.

On the year, Europe's largest economy expanded by a calendar-adjusted 9.4% in the second quarter, leaving economic activity 3.3% below the pre-crisis levels of the fourth quarter of 2019.

The re-opening of the economy and falling COVID-19 cases in early summer have pushed up household spending which translated into booming retail sales in May and June. The economic recovery has also lifted tax revenues, though accumulated tax revenues from January to July are still 1.7% lower compared to the same period in the pre-pandemic year of 2019.

Manufacturing activity remains solid even if held back by bottlenecks in supply chains for intermediate goods. As shown in the chart below, the gap between industrial production and new orders in manufacturing has been widening from the beginning of 2021. The speed of Germany’s recovery is being put at risk as companies in the manufacturing powerhouse report shortages of materials ranging from memory chips to lower-tech parts and even basics such as wooden pallets.

Specifically, construction and car production appear to be particularly hurt by supply shortages (new car sales in Germany were down in August for the second consecutive month).

However, service-sector activity continues to drive the expansion thanks to a loosening of pandemic-related restrictions since May.

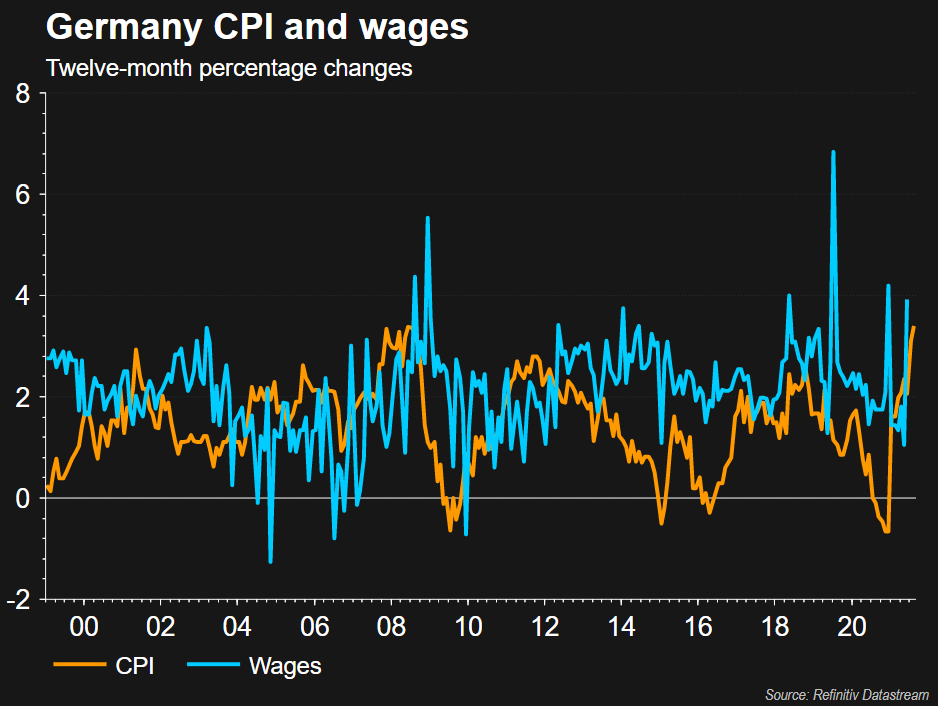

But as we all know, the current star of the German economic scene is the much-feared inflation, which has reached its highest level since 2008. Germany’s harmonised index of consumer prices rose to 3.4 per cent in August from a year earlier, up from 3.1 per cent in July.

What is noteworthy is that inflation is now rising faster than most other European countries due in part to one-off effects, such as the cancellation of last year's temporary value-added tax cut. Nevertheless, according to the Federal Statistical Office, there are few signs that the price pressures are feeding through into wages. In the three months to June, wages including one-off payments rose 1.9% from the same period a year ago. Moreover, the rebound in prices in the pandemic hit hospitality, travel and leisure sectors as well as supply-chain bottlenecks is also pushing prices up in the short term. As a matter of fact, producer prices for German industrial products rose 10.4 per cent in July — the highest increase since 1975 during the oil crisis when headline inflation peaked at a postwar high of close to 8 per cent. Supply chain disruption caused import prices to rise 15 per cent in July, the fastest pace for 40 years.

The key question for markets is whether the rebound in prices will last into 2022. The upside in German inflation in the coming months is likely to be transitory, although there may be potential upside risks in the medium term. For instance, developments in employment will be important to monitor. Signs of increasing tightness in labour markets could determine whether the temporary rise in prices we are seeing turns into something more permanent. While there is little evidence of much wage pressure in Germany (as already reported above), wage growth has traditionally been an important factor in driving core inflation. But for now, annual wage negotiations between the social partners suggest that job preservation considerations are still outweighing demands for wage increases.

The future of German fiscal policy

As specified at the beginning of the previous paragraph, German political forces have divergent ideas regarding the management of public spending and fiscal policy in general. Let's see what may be the points of encounter and clash between the likely coalitions that may arise as a result of the September 26 elections.

Remember: European economic policies in the coming years will depend a lot on the composition of the future government in Berlin. So, let's pay attention to the nuances.

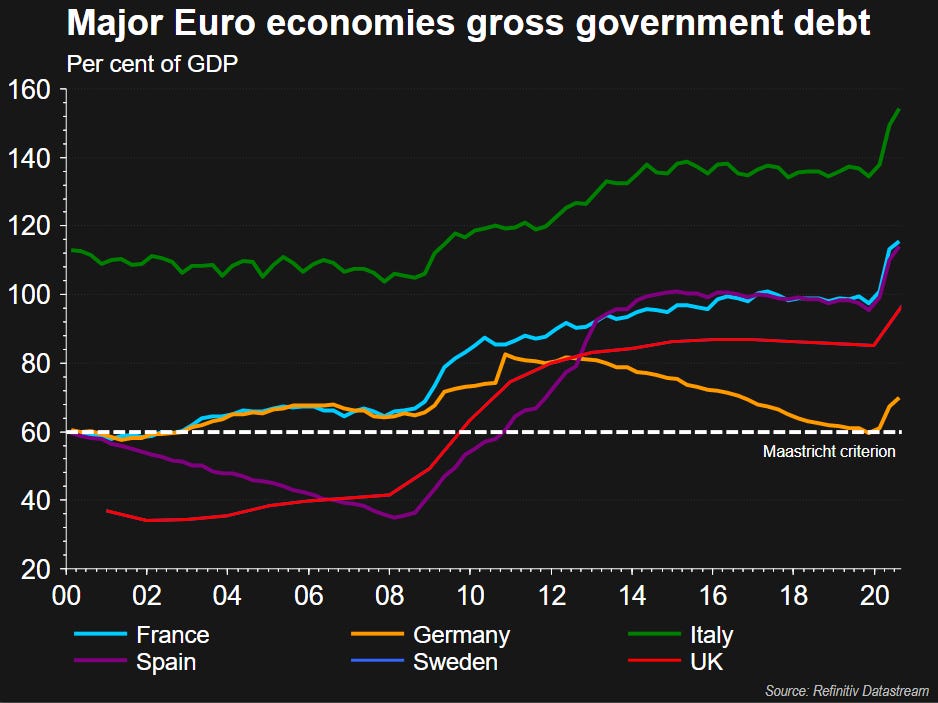

With regard to investments and social policies, in the case of a socialist government the distances with the Greens could be 'manageable'. Both parties would like to introduce a sort of wealth tax and increase investments, perhaps even derogating from traditional German austerity. Translated into European terms, both parties basically agree on the suspension of the Stability and Growth Pact (SGP) until 2023 and in the meantime would like to see an increase in investment, perhaps by derogating from the “debt brake” inscribed in the German Constitution that limits the deficit of public spending to 0.35% of GDP. Indeed, the self-imposed austerity reflects a concern about long-term debt sustainability as an ageing population places an increasing burden on the social-security system and heightens the importance of keeping the debt-to-GDP ratio under control. This could create problems for the center-right parties, who are aiming at the reintroduction of the debt brake (that it caps the federal government’s budget deficits at 0.35% of GDP and forces regional and local governments to run balanced budget) and the debt-to-GDP ratio of 60% at the community level. Moreover, it should be noted that a two-thirds majority in parliament will be required to change the constitutional debt brake. Such a majority is unlikely to emerge after the elections. But an alternative way to increase public spending would be to create off-balance sheet vehicles. This would probably be the path of least resistance for conservative parties.

However, the Greens go even further. They are calling for a review of the SGP criteria to encourage green transition, with some members proposing to make the use of common European debt permanent (in total contrast to the FDP liberals who prefer business support measures in a framework of renewed budgetary rigour for Germans and the EU).

The composition of the coalition that will emerge following the September elections will play a fundamental role in the future of European fiscal rules. In fact, while EU fiscal rules remain suspended until 2023 because of the pandemic, the European Commission is due to deliver a report on their reform by the end of this year. Depending on the coalition, the fiscal space of the Eurozone's largest economy could change.

Despite various divergences, there seems to be a broad consensus on the need for more public investment. Why? Because the current crisis – as well as the first decade the debt brake’s application – has exposed critical limitations that should allow for a serious political debate on how to reform the German and, eventually, the European fiscal framework. Revising the debt brake, which governs the operation of the rule and German fiscal federalism, would require amending Germany’s constitution and would entail securing a two-thirds majority in the Bundestag.

Key takeaways

The debt brake has probably played a role in strengthening Germany’s fiscal position even though fiscal consolidation preceded its introduction. But a framework resting on unobservable data such as the structural balance and output gap is prone to procyclicality, revisions, and mismanagement. The consistent overperformance of fiscal rules from Germany’s federal government is not a sign of success, but rather a sign of consistent bias in the operation of the rules.

The debt brake has also profoundly undermined Germany’s public investment. It has considerably weakened its ability to act in the face of crisis, modernize its economy, and allow for an effective climate and energy transition.

The September 26 elections will play a major role in fiscal policy at the European level. A return to existing EU fiscal rules (driven by German center-right parties) would mean countries on the EU periphery having to significantly consolidate their public finances, which could undermine the path to recovery. On the contrary, greater fiscal accommodation pushed by a virtuous country like Germany (driven by the Socialists and the Greens) could benefit peripheral countries.

The Macro Code is an open diary on markets, macro-trends and structural changes.

To receive updates in newsletter format, follow the form below.

Please, note that The Macro Code represents personal views only.