The Macro Code #8 – Pt.1: Possible Inflation Drivers?

Chipflation, Foodflation, Gasflation, Wageflation, Greenflation

Welcome to The Macro Code, an open diary on markets, macro-trends and structural changes.

Inflation, like aircraft, has two main drivers. The first reflects business cost pressures (whether wage-related or related to the price of intermediate goods); the second driver is short- and long-term expectations.

This week's newsletter is divided into two episodes.

Episode 1 - available below (referring to the first driver of inflation): Let's have a recap on global inflation dynamics, with a specific focus on bottlenecks along production chains and supply constraints, starting from energy and raw materials and ending with intermediate products (such as micro-chips) and then final products (e.g. cars or technological devices).

Episode 2 - available at the end of this week (referring to the second driver of inflation): We try to understand how useful future inflation expectations are in order to price current inflation. More specifically, we ask whether inflation expectations are useful for getting an estimate of the transience of the current price rise.

Cost pressures

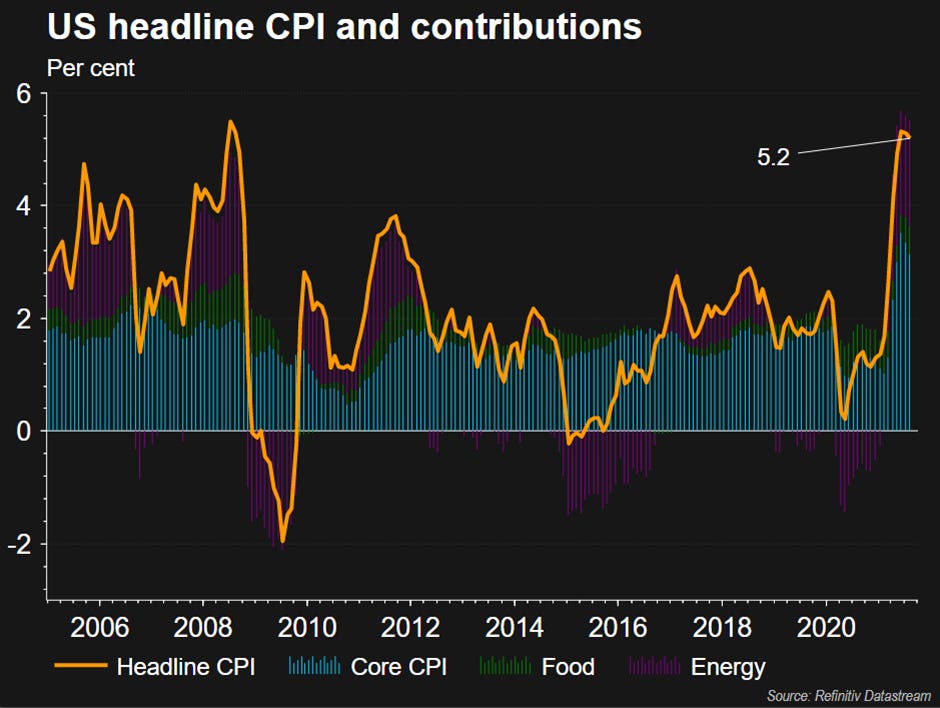

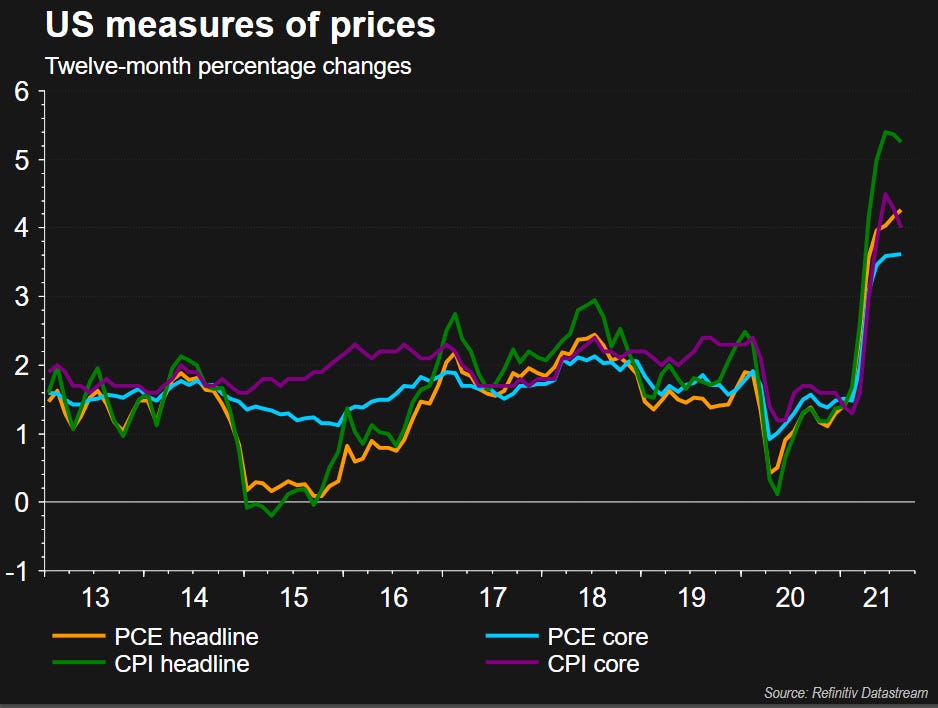

It is becoming increasingly apparent that the pick-up in inflation, particularly in the US (last week, the U.S. CPI recorded a figure above 5% for the fourth time in a row), is cyclical and not transitory.

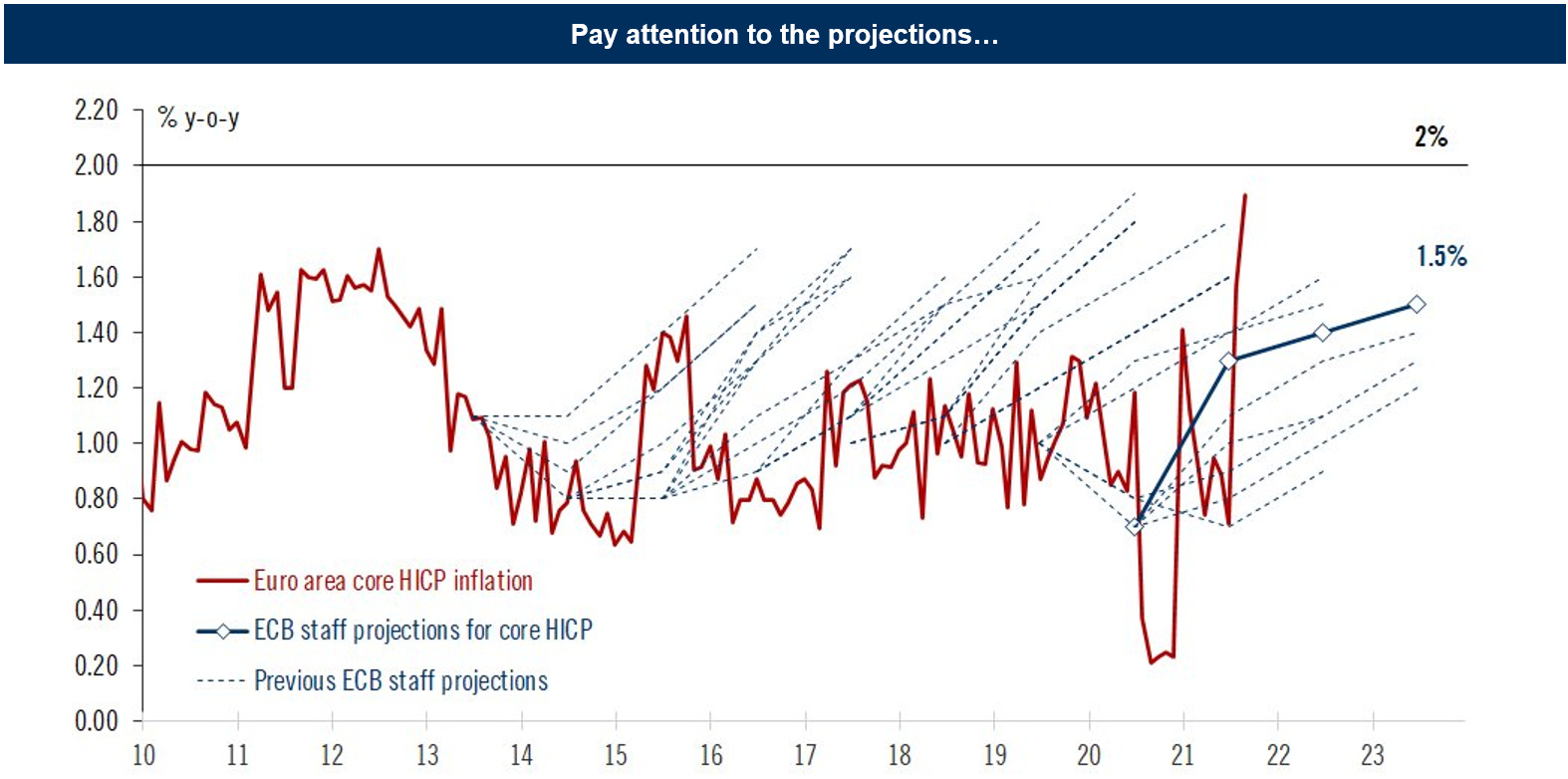

It is not just a consequence of base effects. As noted in the chart below, core inflation is no longer about base effects and momentum is very high in many countries (and well above the 2% targets).

Traditionally, any cyclical pick-up in inflation has required a monetary policy response. But that is not the intention of policymakers at present.

In the US, many FOMC members continue to believe that the pick-up will be transitory. The market has doubts about this. Inflation overshoots driven by a spike in the oil price and energy prices, by a change in tax rates, by a shortage of raw materials, or by a depreciation of the currency, tend ultimately to subtract from household real incomes. In that sense, they can be self-limiting, and deflationary in the long run, and it is often appropriate for policymakers to look through them. But that is not what we are seeing here. Only in the unlikely event that higher product prices do not feed through at all to higher wages, which would require a very strong degree of faith in policymakers’ ability to rapidly bring inflation back to target, would a cyclical pick-up in inflation be self-limiting.

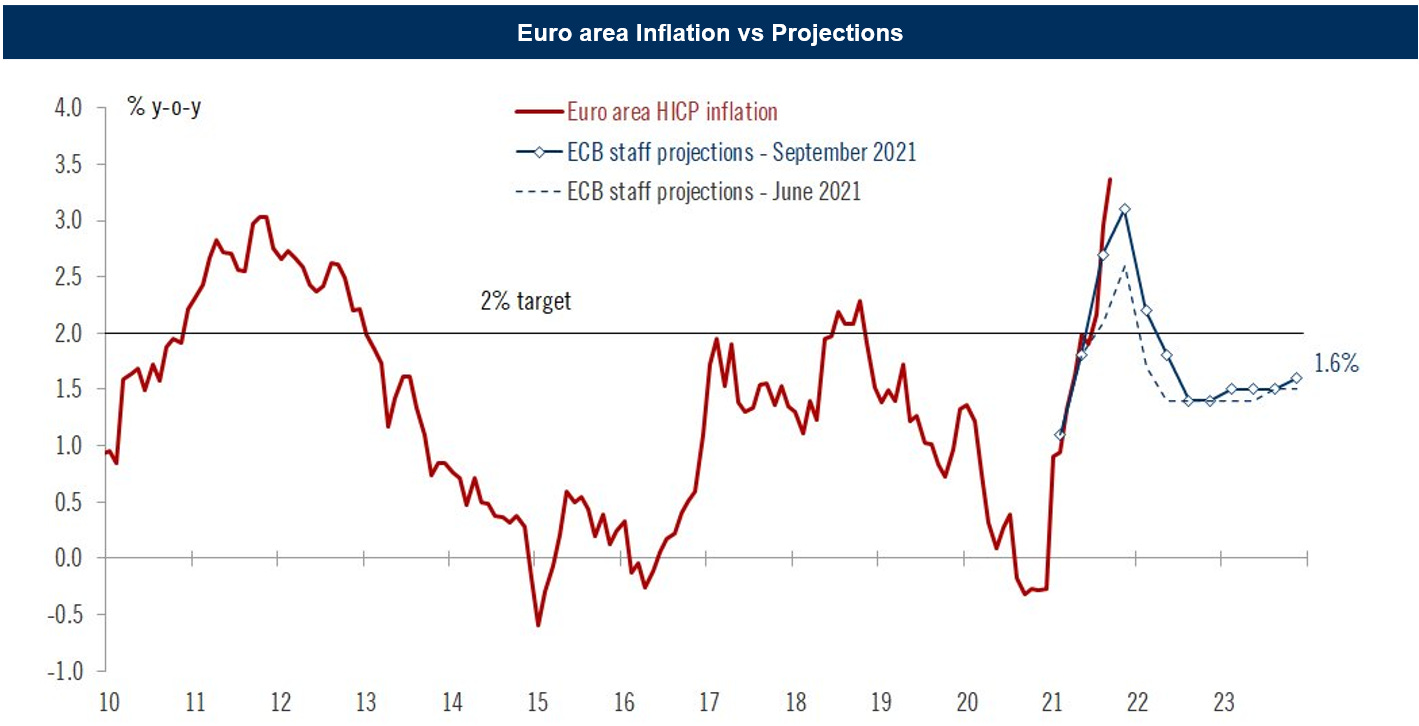

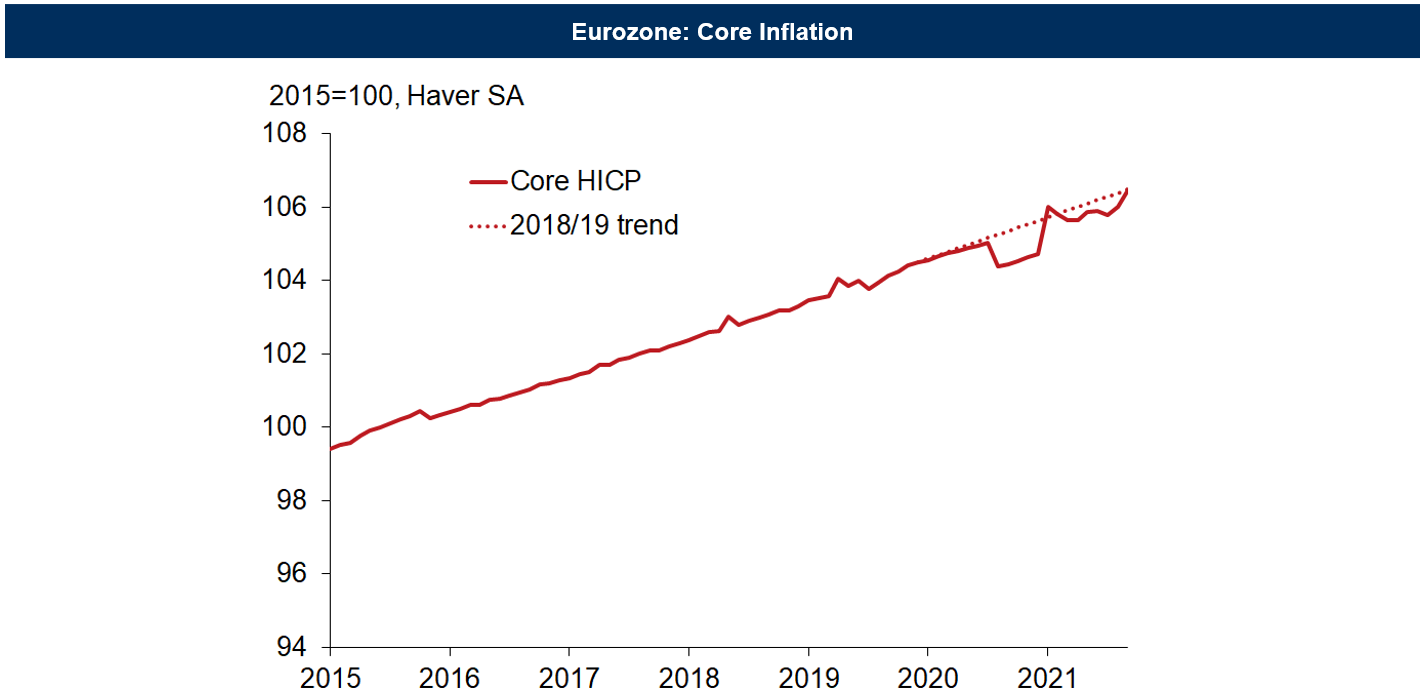

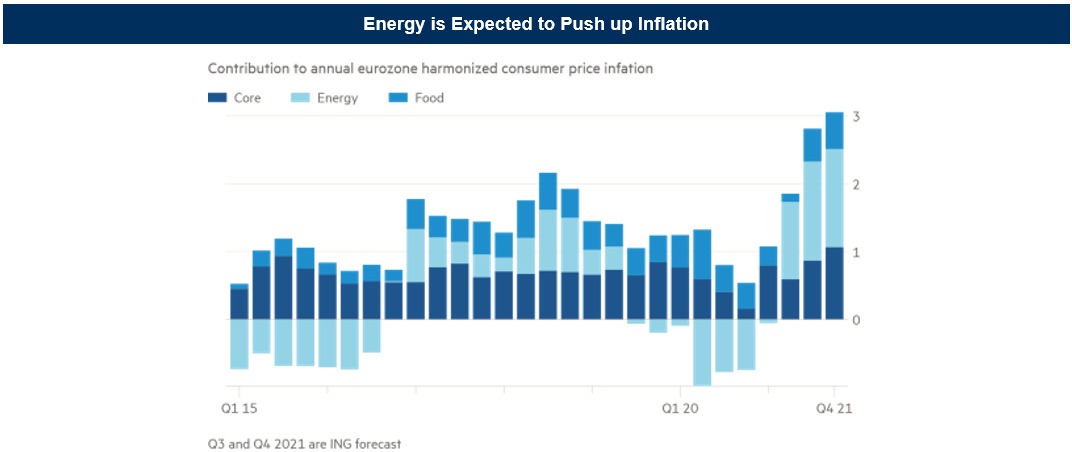

In Eurozone, the Euro area flash HICP inflation rose to 3.4% in September, pointing to upside risks to ECB staff projections. Core inflation up to 1.9%, highest in 13 years, on reopening effects.

As Pictet AM points out, transitory - but higher for longer inflation - will create some communication problems for the ECB.

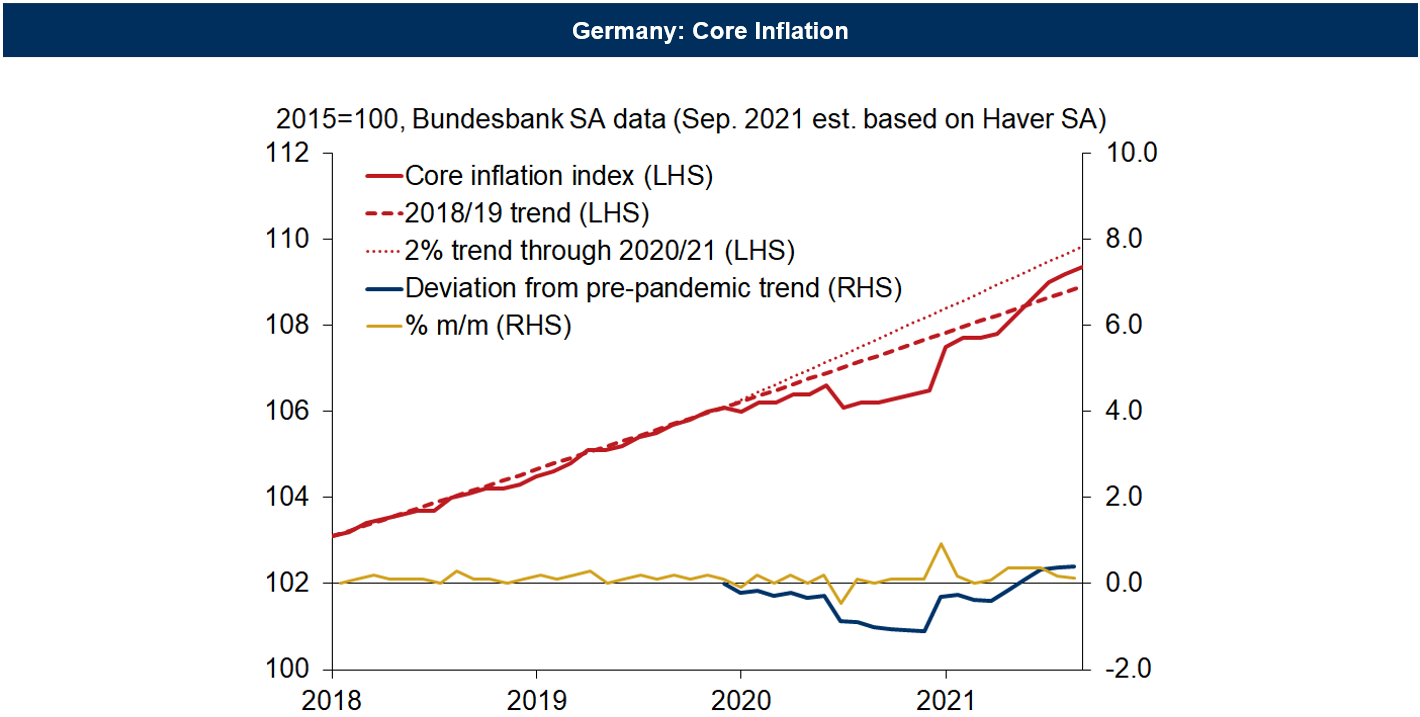

As a consequence, core inflation will likely rise slightly further, especially in Germany, with base effects peaking around November. Staff projections will be revised higher. The ECB forward guidance criteria aren't met yet. The reduction of core inflation close to, but above 2%, will help the hawks.

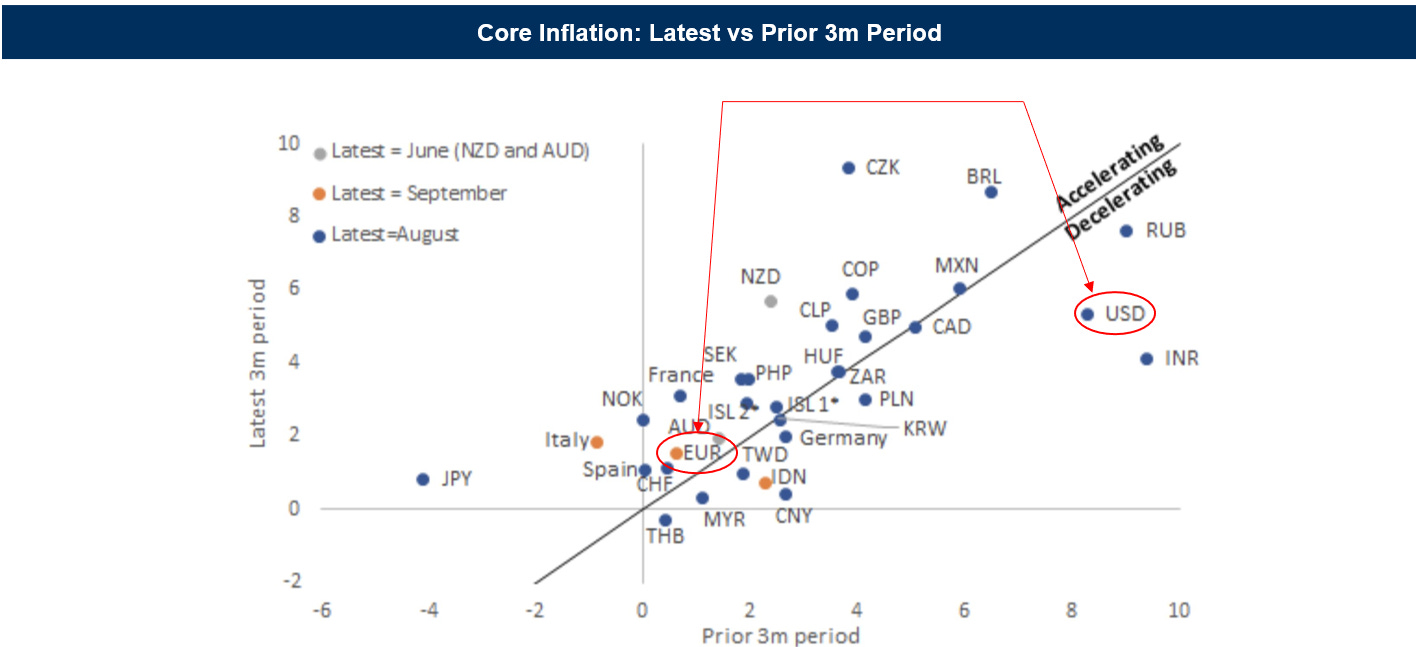

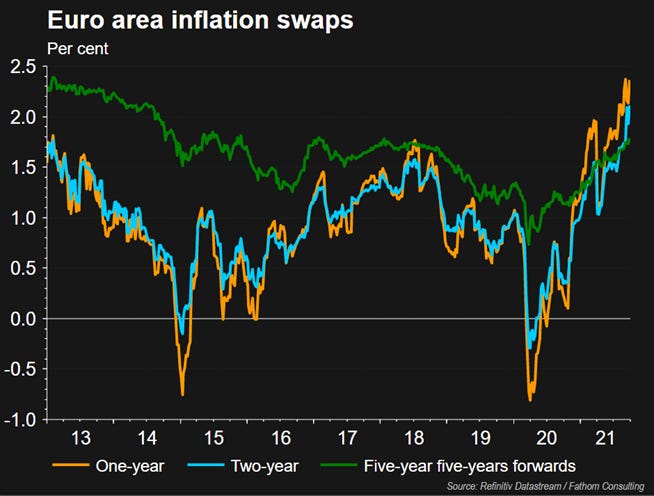

In spite of this, the rise in prices is much more marked and lasting in the US than in the Eurozone (see the red arrows in chart number two).

For example, according to Oxford Economics it should be noted that headline inflation in Germany is at 4% y/y, but core inflation probably saw the smallest monthly increase in six months in September.

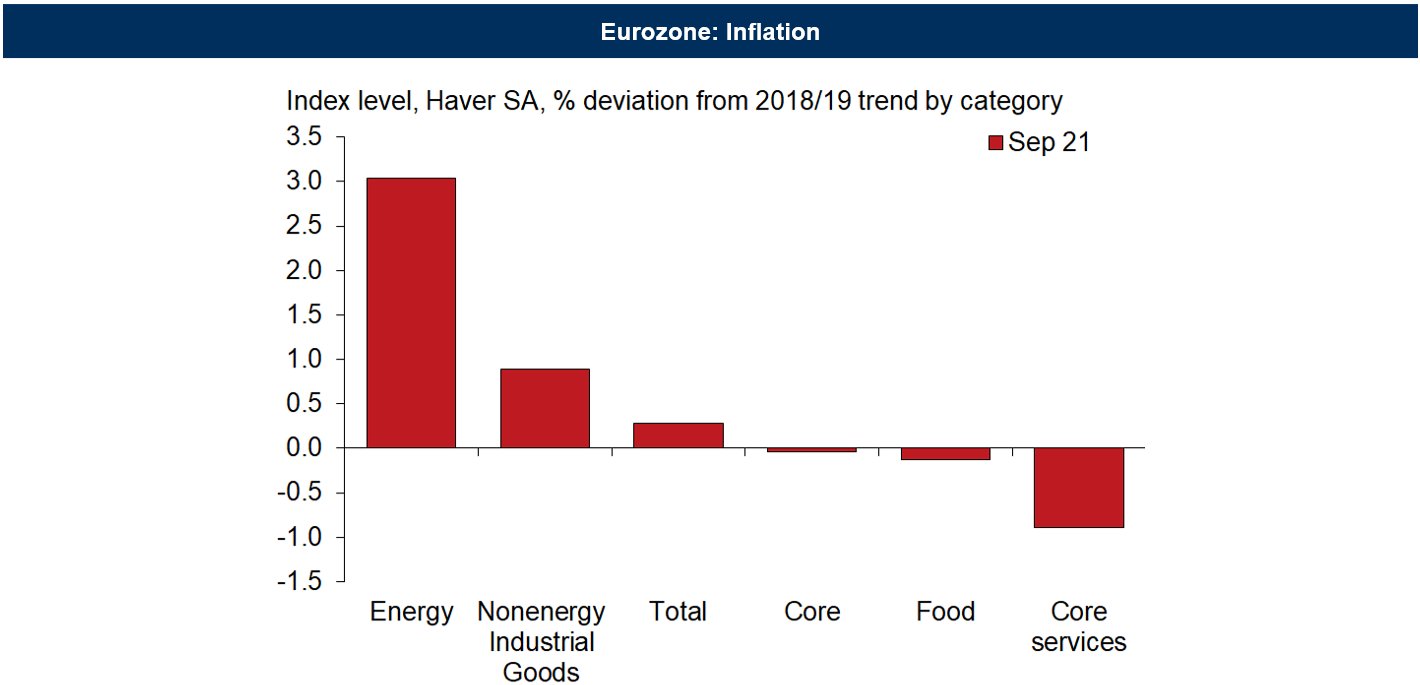

Moreover, lifted by robust demand and severe supply-bottlenecks non-energy goods prices have pushed the eurozone core CPI back to its pre-pandemic trend in September. Services inflation also continues to recover partially due to base effects, but the price level remains well short of the trend.

Differences in inflation trends between the U.S. and the Eurozone are evident, but overall the price level is trending upward. This trend may be increasing faster than expected, calling into question the idea that inflation will prove to be transitory.

Consequently, it is legitimate to ask what factors are impacting this bullish dynamic.

The 5 drivers driving the inflation debate

Chipflation

Foodflation

Gasflation

Wageflation

Greenflation

Chipflation

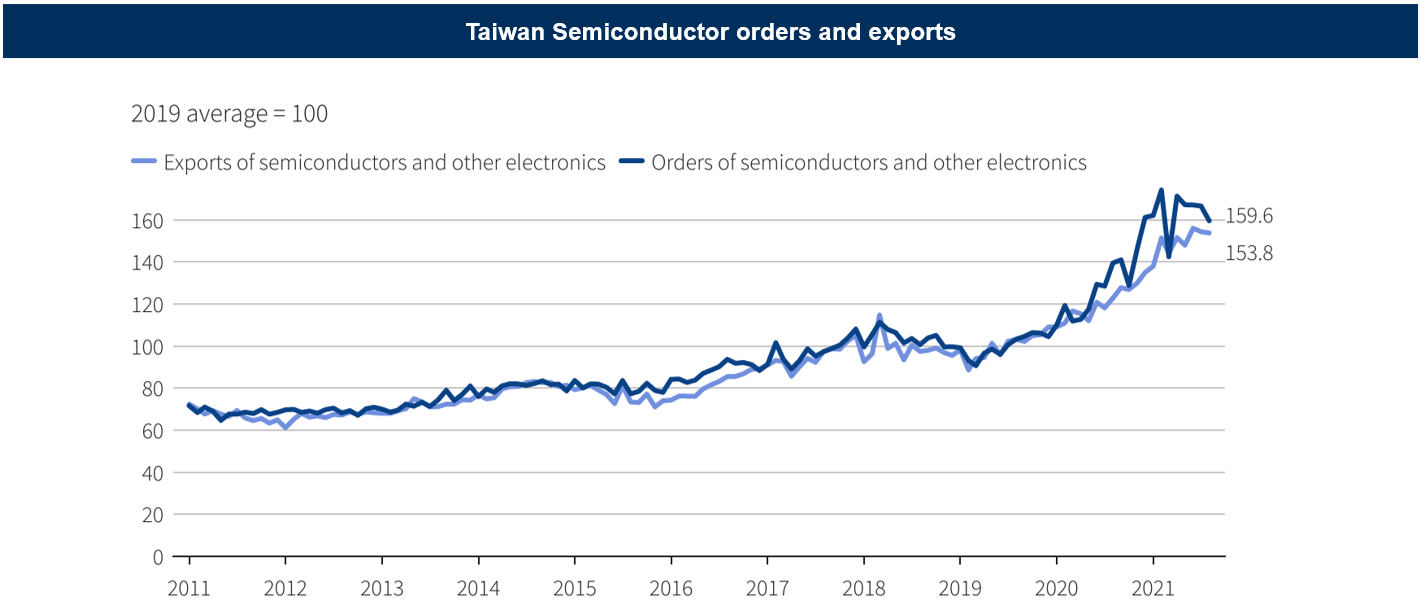

Understanding the dynamics of the 2020-2021 global chip shortage is relatively simple: the demand for integrated circuits (commonly known as semiconductor chips) is greater than the supply.

The cause of the global chip crisis is a combination of different events with the snowball effect of the COVID-19 pandemic being the primary reason. Other causes have been attributed to the China-United States trade war and the 2021 drought in Taiwan.

Taiwan is the leader of the global semiconductor industry, with TSMC alone accounting for more than 50% of the global market in 2020. In 2021, Taiwan experienced its worst drought in more than half a century, leading to problems among chip manufacturers that use large amounts of ultra-pure water to clean their factories and wafers. For example, TSMC's facilities used more than 63,000 tons of water a day, more than 10 percent of the supply of two local reservoirs.

For this reason, Taiwan Economy Minister Wang Mei-hua said that solving the global shortage of auto semiconductors needs Malaysia's help, especially when it comes to packaging. The problem was especially acute with auto chip packaging, with companies in Malaysia providing services not offered by Taiwanese firms.

In fact, the effects on the automotive sector are significant. In Europe, premium car brand Audi (Volkswagen's biggest profit contributor) has to troubleshoot on a day-to-day basis to tackle an ongoing shortage of auto chips, its chief executive said.

Along the same lines in the US, General Motors and Ford will cut additional production because of the nagging semiconductor shortage that has hit global auto production.

Foodflation

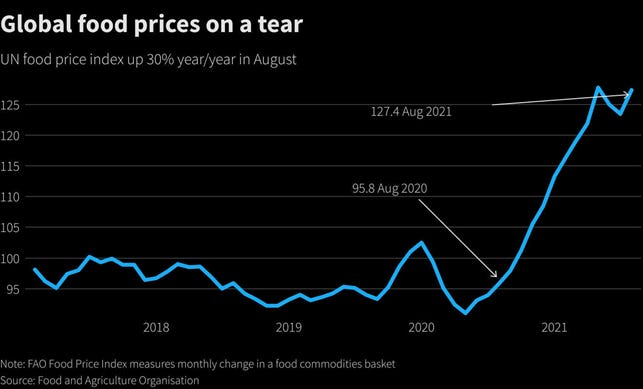

An aggregate index compiled by the UN Food and Agriculture Organisation shows that global food prices rose 30% y/y in August.

While higher agricultural commodity prices are behind the jump, JPMorgan analysts also attribute food price inflation to pandemic-related pressures such as logistics disruptions and transport costs.

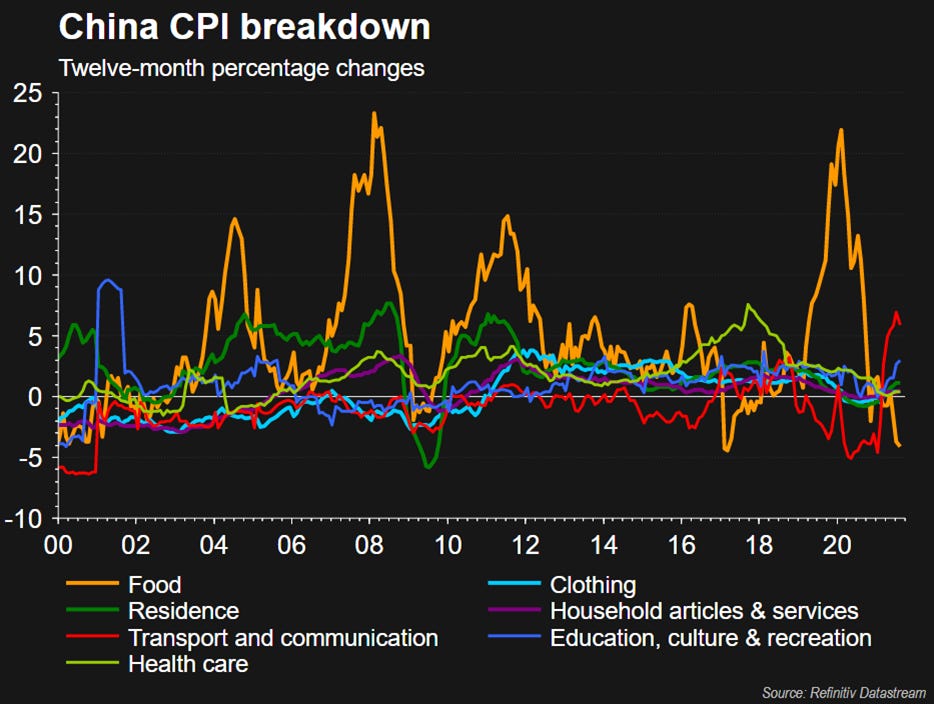

In emerging markets, where food makes up a large chunk of inflation baskets (see chart below), there is more pressure to tighten monetary policy. It is less of a problem for developed nations but price rises look inevitable for items such as soft drinks and snacks.

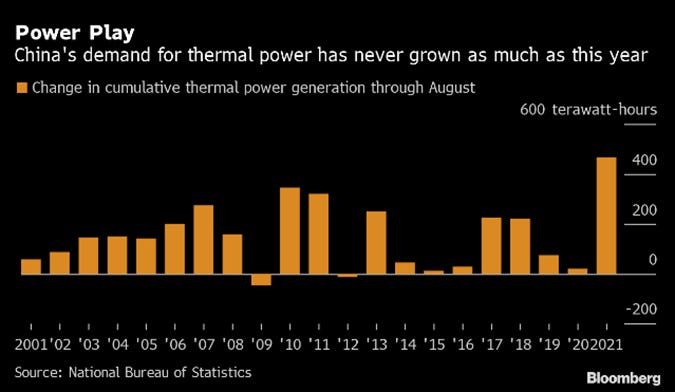

In addition, global food prices (which have fallen from their peak in recent months, but remain historically high) could rise again due to China's energy crisis.

In fact, China is facing a challenging harvest season due to a major energy crisis.

Beijing is struggling to secure energy supplies and restore electricity with the fall harvest underway in the world's largest agricultural producer.

Regions among the hardest hit are northeastern provinces such as Jilin, Liaoning and Heilongjiang, where about half of China's corn and soybeans are produced. In recent weeks, several plants have been forced to shut down or reduce production to save electricity, such as soybean processors that crush beans to produce flour for animal feed and oil for cooking.

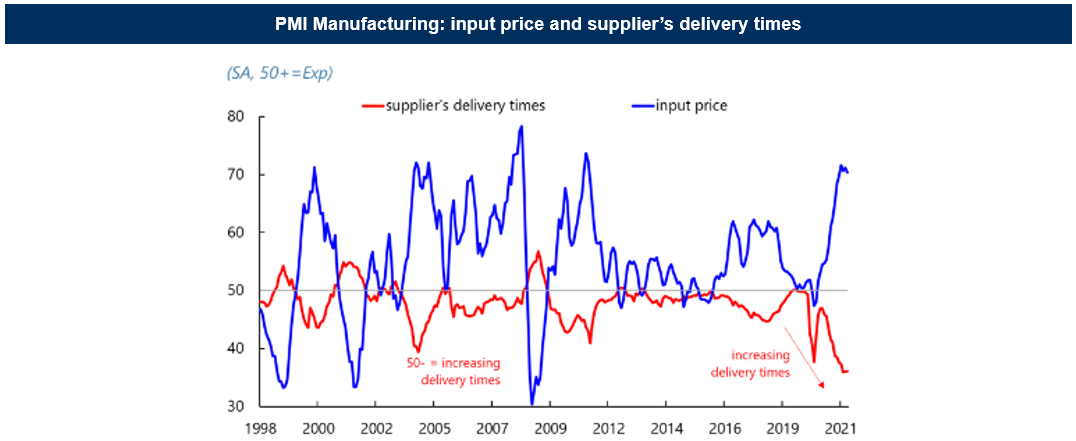

Another key point of relevance in the food supply chain is that of longer supply times. An IHS Markit survey of delivery times indicates historic delays: congestion at ports appears to be a now-relevant factor that has had longer-than-expected transience.

Gasflation

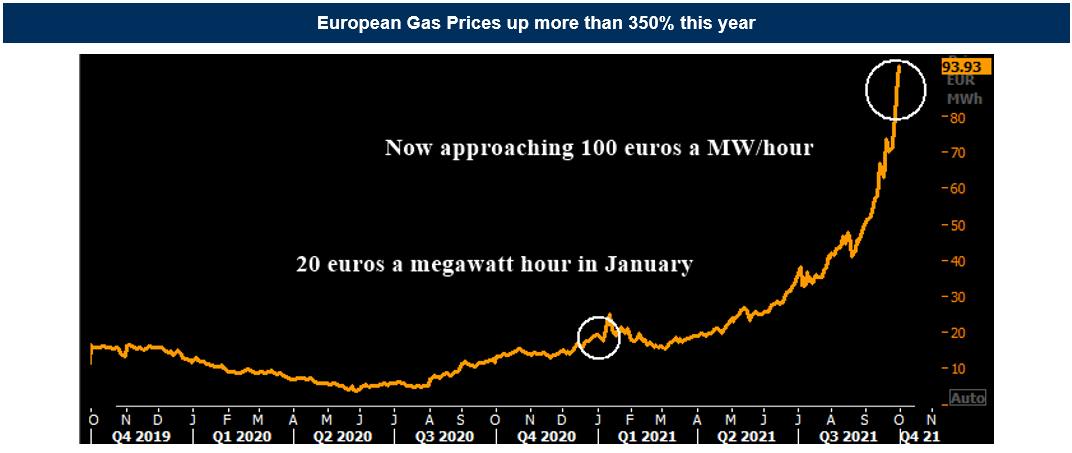

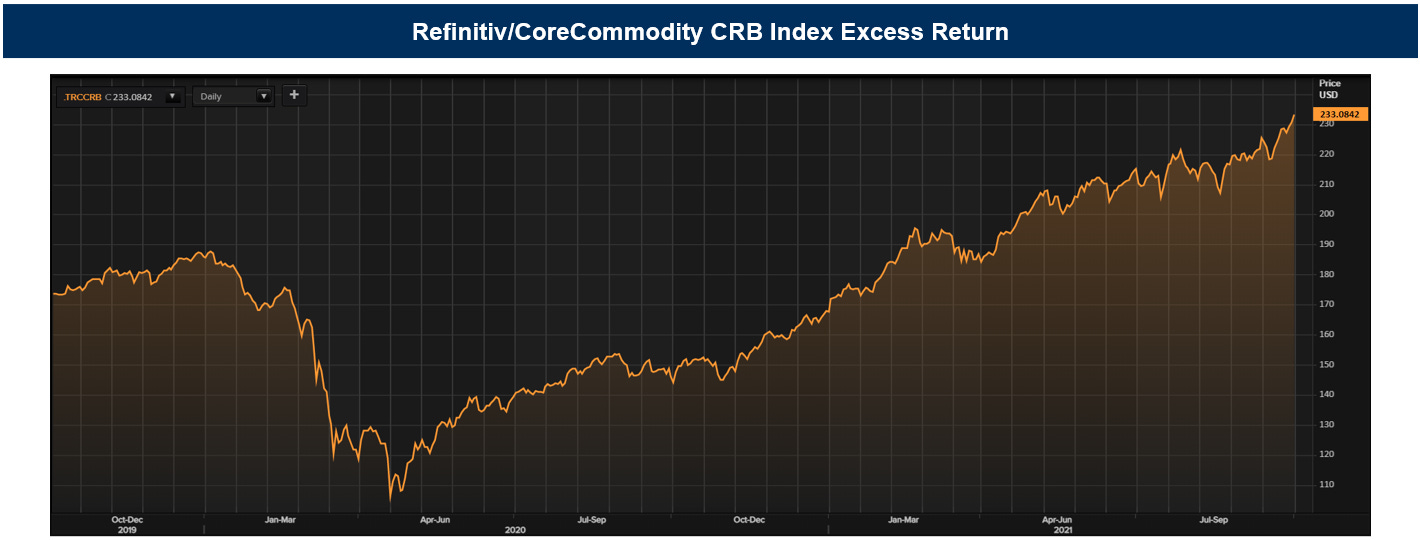

A deep energy crisis adds to the list of supply chain bottlenecks. Production disruptions in the Nordics and reduced flows from Russia are limiting natural gas supply across Europe. The shortage is particularly deep in the U.K., where a Brexit-induced shortage of truck drivers is exacerbating the problem. News of the shortage has brought unrest to both governments and citizens, further fueling price pressures. As a result, energy prices have skyrocketed: natural gas prices have doubled in the past month and quadrupled since April. The crisis is gradually affecting all commodities, with Brent crude up 20% from its August lows.

In the first two quarters of the year, Bloomberg’s general commodity price index rallied more than 20%, largely driven by the rise in energy prices (44.5%), followed by the less pronounced but nevertheless important increase in agricultural goods (20.5%) and industrial metals (17.6%). The rally is due to a combination of demand-side factors (economic reopening, with a particularly strong revival in the industry), supply-side factors (reduction in inventories), and financial elements (increased appetite for risk and depreciation of the dollar).

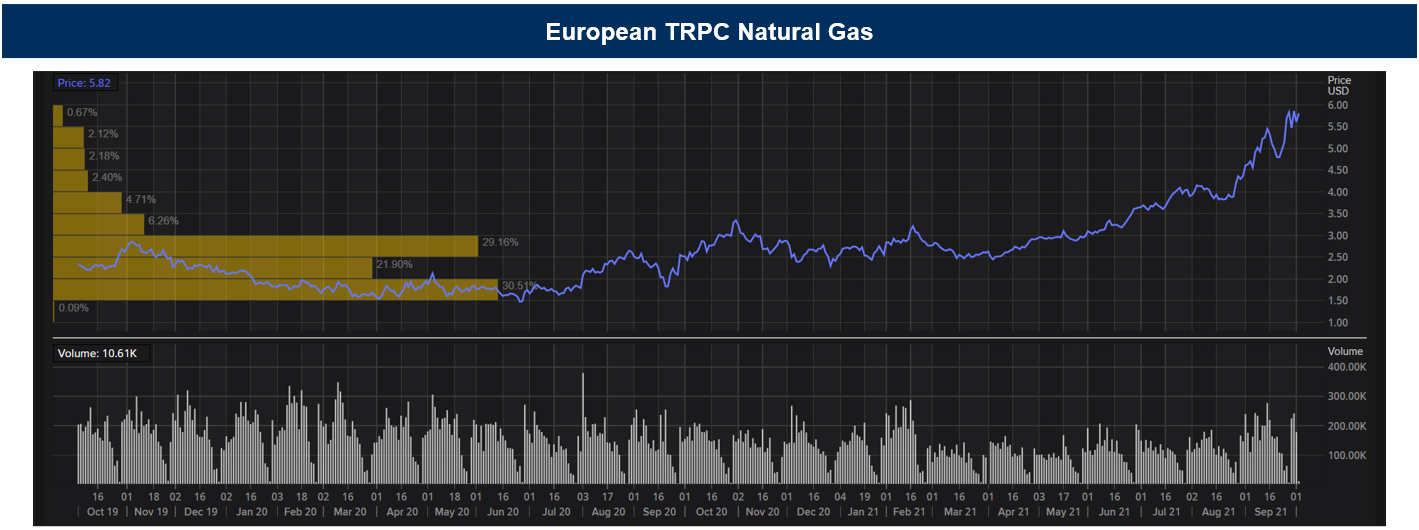

If we focus specifically on gas, we see that the European TRPC Natural Gas and NYMEX Henry Hub Natural Gas prices have soared more than 350% and more than 120% respectively this year.

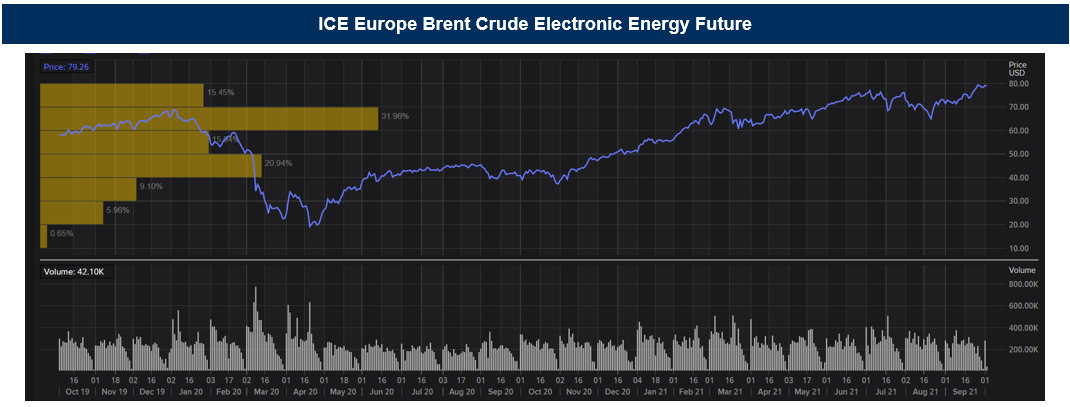

ICE Europe Brent Crude Electronic Energy Future is up around 50% and Goldman Sachs expects Brent crude to hit $90 a barrel by end-2021 from around $80 currently.

Gas and electricity make up 4.8% of the euro area harmonized-inflation (HICP) basket used by the European Central Bank.

Higher energy bills would also hit household budgets and consumer confidence, threatening the economic recovery. Considering that energy accounts for nearly 10 percent of consumer spending in Europe, a double-digit annual increase in energy prices could have a significant effect on economic recovery.

The impact of rising energy prices extends beyond the EU. In August, the annual rate of energy price inflation increased by more than 60 percent in Norway, exceeded 20 percent in Canada and the United States and saw double-digit increases in South Korea, Chile, and Mexico.

Many economists see higher gas prices as here to stay, due to slowing U.S. output, rising costs of carbon emissions permit for polluters and curbs on the usage of dirtier fuels.

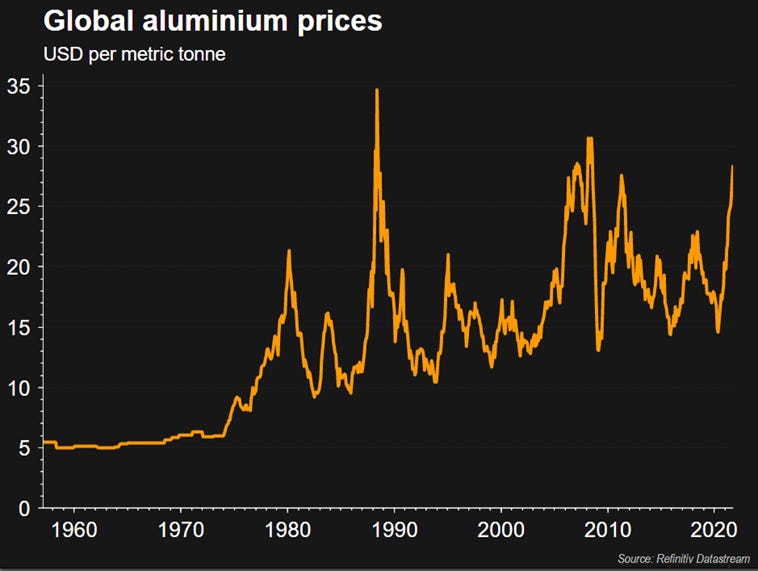

In China, where factory inflation hit 9.5% in August, power cuts have slashed the output of goods from cement to aluminum.

These outages are a risk to end-users such as those in auto supply chains.

Although energy represents a large weight in the inflation basket, most energy contracts are regulated. This protects consumers if increases are transitory. However, when the pricing in contracts expires, gas inflation will become tangible in utility bills, negatively impacting overall price levels and consumer purchasing power.

Hopefully, it won't be too cold a winter.

Wageflation

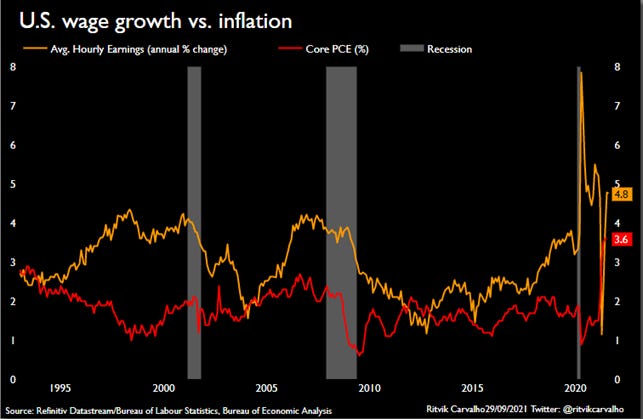

The economic system functions as the human body. There are multiple connections between vital organs, just as there are between economic variables. Indeed, the confluence of inflation, labor shortages, and immediate need for workers has resulted in “wageflation” — a precipitous, unexpected, and immediate rise in wages based on unique market forces. With wageflation, employers pay more for the same job and the same level of productivity.

As prices rise, so do expectations of future inflation among consumers, who consequently demand wage increases.

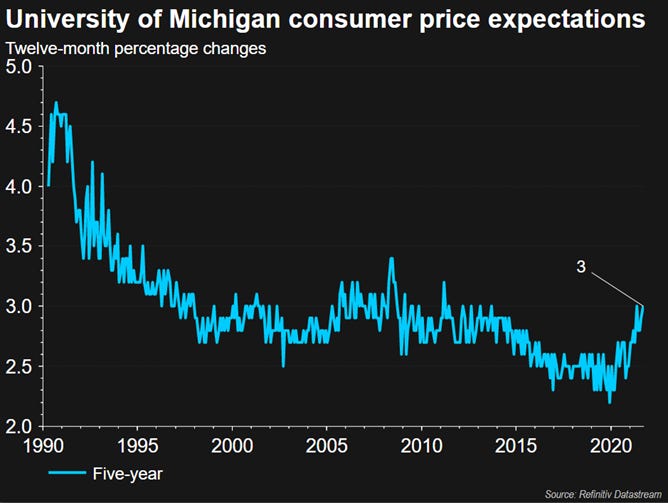

Globally, the wage growth picture is mixed. U.S. average hourly earnings rose 0.6 percent in August and five-year U.S. inflation expectations hover around 3 percent, according to surveys.

In some sectors in the UK, earnings have increased by up to 30% this year.

Eurozone labor costs declined in the second quarter, but inflation and inflation expectations are rising.

Greenflation

As noted by Ruchir Sharma, the world faces a growing paradox in the campaign to contain climate change. The harder it pushes the transition to a greener economy, the more expensive the campaign becomes, and the less likely it is to achieve the aim of limiting the worst effects of global warming.

New government-directed spending is driving up the demand for materials needed to build a cleaner economy. At the same time, tightening regulation is limiting supply by discouraging investment in mines, smelters, or any source that belches carbon. The unintended result is “greenflation”: rising prices for metals and minerals such as copper, aluminium and lithium that are essential to solar and wind power, electric cars and other renewable technologies.

Prices for European carbon allowances have doubled this year to 65 euros a ton. A price of 100 euros would increase retail electricity prices in Europe by 12%, adding 35 bps to headline inflation in the eurozone, Morgan Stanley estimated in June.

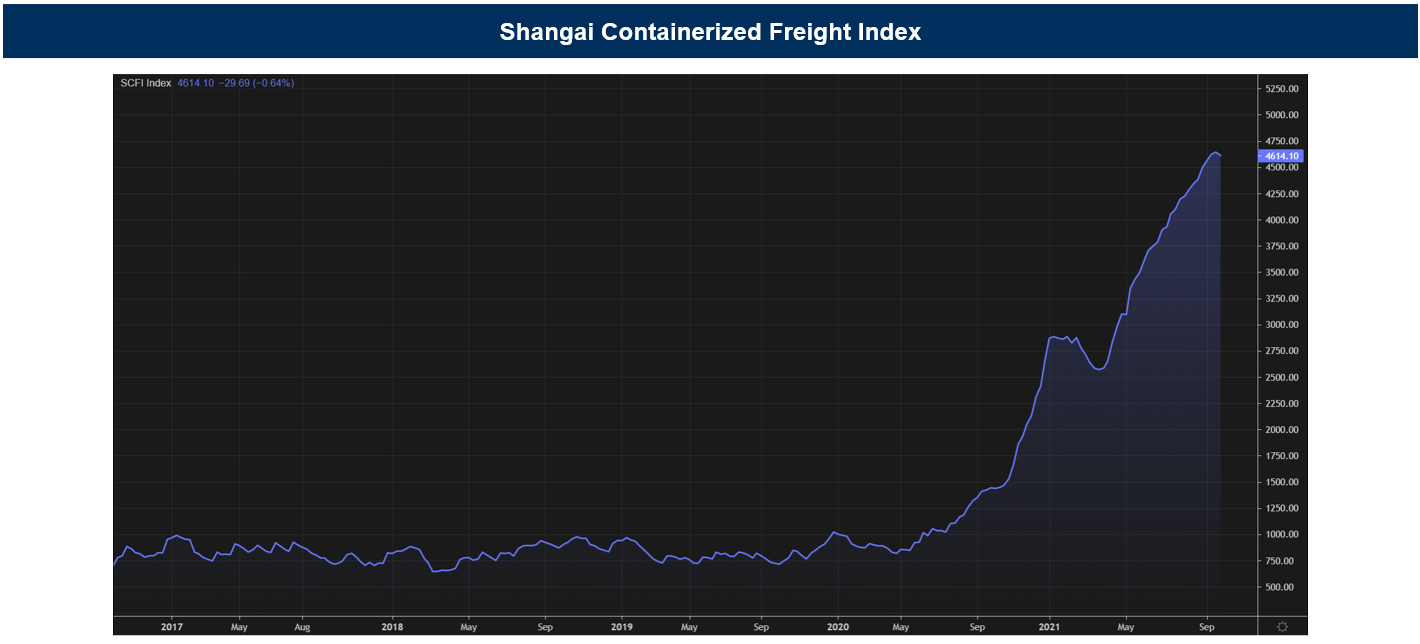

There are other examples. Declining ship orders due to impending fuel rule changes could be a tailwind for shipping rates that have already risen 280% this year.

In the green transition process, we are missing steps. In fact, two of the most important metals for green electrification are copper and aluminum. But investment in these metals has been depressed by companies to comply with environmental, social and governance issues. However, the bottom line is that the world needs more copper to stop global warming. Aluminum is one of the dirtiest metals to produce, but it's also one of the most vital metals for solar power and other green energy projects, and, according to the World Bank, it's set to face a particularly sharp increase in demand in the coming decades.

In this process, China's role as a major supplier of raw materials has also been turned upside down. A decade ago, the country was still producing raw materials such as iron ore and steel and dumping the excess on foreign markets. Now Beijing has cut production as part of its campaign to achieve carbon neutrality. Nearly 60 percent of aluminum comes from China, which recently shut down new smelters because of its fat carbon footprint.

In episode number 2 of this weekly newsletter from The Macro Code (available later this week), we'll talk about how good inflation expectations are for pricing in current inflation.

In such an uncertain environment, these two episodes complement each other.... don't miss it!

The Macro Code is an open diary on markets, macro-trends and structural changes.

To receive updates in newsletter format, follow the form below.

Please, note that The Macro Code represents personal views only.