The Macro Code #6: Is Evergrande a Lehman event? The Minsky Moment is here.

Are we facing a Minsky Moment within the Chinese market?

Welcome to The Macro Code, an open diary on markets, macro-trends and structural changes.

The entire financial community is holding its breath in the face of the difficulties of Evergrande, a veritable corporate giant not only in terms of its financial size but also in terms of the ramifications of power it conceals. Many investors are analyzing the systemic consequences that could overwhelm the markets following the bankruptcy of the primary Chinese real estate player. There are alarmist currents (a new Lehman event), denialist currents (state intervention will fix everything)... clarity is needed.

One fact is for sure: interpreting the Evergrande Moment is a difficult task. Many are wondering if it will be a Minsky Moment (when trust is broken after a long period of speculation), similar to the Lehman collapse. Or will it be more like the LTCM Moment (in reference to the failure of the famous LCTM fund in 1998, which was followed by a sudden loss of confidence after a period of excessive speculation)? Or, alternatively, it could just be a less important event altogether. To measure this, we need to resuscitate another concept that many of us thought we had heard the last of more than two decades ago: the Asian contagion.

The keyword driving this newsletter is "contagion."

The goal of this newsletter is twofold:

To take a closer look at the macro causes and consequences of Evergrande's financial woes. We will try to think about both what is happening below the surface (the bond market) and above the surface (the Chinese authorities' regulations to curb leverage).

Understand what has been happening in China in recent months at a general level and to what is due the overlapping of sudden and unexpected decisions that upset the hitherto very accommodating structure of relations between political power and certain business giants.

Evergrande: what happens below the surface?

Evergrande Group is by sales the second-largest real estate development company in China. In 2018, it became the world's most valuable real estate company. In August 2021, the Financial Times reported that Evergrande Group is facing a record number of cases filed by contractors in Chinese courts as pressure mounts on the company's management to reduce its $300bn in liabilities, including around $100bn in debts. In mid-September 2021 it was reported that the company was in danger of being unable to issue payments on loan interest due on 20 September. It was estimated that around 1,500,000 customers could lose deposits on Evergrande homes that have yet to be built if the company goes under. Based on these deep credit difficulties, the markets proceeded to dump the stock without delay.

On September 20, after mainland China's markets closed for the vacation, Hong Kong woke up hit by the crisis. The Hang Seng Chinese Enterprises Index hit a low after the close of last year's pandemic.

The uncertainty will continue for a few more days as China is in a period of intense festivities.

Volatility in global markets has returned (also aided by the expected Fed meeting on Wednesday, September 22), with the VIX index jumping 34% to its highest level in over four months.

The Chinese market faces the problem that Evergrande is a landmark real estate company with over a thousand projects across the country and total liabilities of over $300 billion. A default could pose financing problems for Chinese real estate companies and the Chinese banking sector, which has inevitably increased its exposure to the real estate giant over the past decade.

Refinancing debt in the onshore market will be very problematic due to low demand.

Refinancing in the offshore market would also be impractical due to the recent increase in financing costs for Chinese high-yield USD companies. According to Bloomberg Barclays indices, yields have risen from around 8% in May to 13.70%, the highest level since March 2020 when the Covid-19 pandemic was hitting the market.

Evergrande's onshore bond trading has been suspended (see here) for one day (last September 16th). The statement issued by Hengda Real Estate Group Co Ltd (China Evergrande Group's main unit) explained that the suspension of trading is to inform all investors of the company's downgrade to A from AA, which for China Chengxin International is the lowest investment rating. This is a move that prevents small investors from making speculative investments.

The composition of credit ratings for Evergrande has become critical, with revisions on outlooks in mid-September quite negative by major international rating agencies.

Some are expecting that bonds will not resume trading at all and will be equitized. This has explained the 8% plunge in equities, bringing bonds to a 0 lane.

Things are different for offshore US dollar bonds, which trade around thirty cents on the dollar. The first bond to mature is the Evergrande 8.25% March 2022 (XS1580431143). Although the company has no bonds maturing this year, the company was due to pay interest next week of $83.5 million on a one-dollar bill and $36 million on a local bill. Hopes of payment have now evaporated as Chinese authorities have told lenders not to expect interest payments next week.

At this point, there are two scenarios for bond investors:

Restructuring: Optimal solution for investors, although analysts expect US dollar debt to be cut by about 70%.

Liquidation: A major danger for bondholders. It would take a long time to liquidate all assets and equity investors would probably receive nothing.

Globally, the repercussions of these two scenarios may be manifold for a variety of reasons.

According to Bank of America, Evergrande is the largest issuer of high-yield dollar bonds in China, accounting for 16% of outstanding bills. If the company were to collapse, this alone would push the default rate on the country's junk dollar bond market to 14% from 3% (Evergrande makes up 10% of China's offshore HY market). Such a spike in the default rate could spill over to the rest of the High Yield market in China, other emerging market countries but also advanced economies.

A collapse would force banks to cut their holdings of corporate bills and even freeze money markets, which serve as the plumbing of China's financial system.

Evergrande's debt concern comes at a time when China's economy is slowing sharply. This could have negative consequences for global growth.

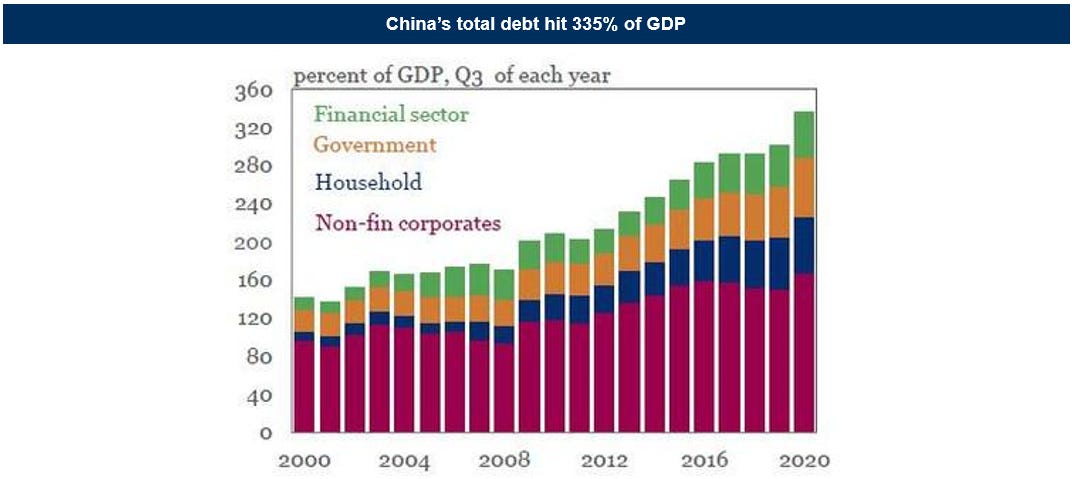

Evergrande's critical situation represents a threat to the Chinese debt bubble: as can be seen in the chart below, the Chinese economy is highly indebted. The debt/GDP is already well above 350%, a level where if it does not continue to grow exponentially it ensures some serious problems.

As a result, given that most of China's large debt burden is on the balance sheet of companies like Evergrande, contagion risk essentially depends on three factors: 1) How "funded" the Chinese economy is; 2) the size of foreign leveraged long positions on Chinese products; 3) CCP reaction: credit creation or debt reduction? (as noted by @Macroalf here).

Evergrande: what happens above the surface?

As an introductory note, it should be specified that when discussing Chinese economic issues, uncertainty reigns supreme. Outside observers are deliberately kept in the dark on many parameters by the Chinese authorities (e.g., Tom-Tom GPS data used in Chinese cities has been blocked - probably - by Chinese regulators, which makes it difficult to assess levels of economic reopening and true development.

However, even if we do not have a large real-time dataset, there is nothing to prevent us from trying to figure out whether Evergrande's default can be likened to a new Lehman case.

First, we note that Evergrande can be seen as a bellwether for Chinese credit growth.

Although there are numerous alarm bells about the fate of Evergrande, there are several signs that tend to suggest that we are not facing a Lehman scenario.

Probably, as Nordea's latest newsletter points out, Evergrande's is a drama but not that dramatic. The chart below shows that bond markets have yet to worry about various spillover effects, for example in the tradable bonds of Country Gardens (China's largest real estate developer). This suggests that the Evergrande event is one that is still not fully contextualized.

Plus, as this chart produced by Societe Generale SA shows, there has been no contagion from high yield to investment-grade debt.

But still, the differences with the Lehman case are striking.

In fact, China is not yet organically connected to the world financial system, as the United States is. It has a series of watertight compartments and the currency is not convertible so there can't be capital flight. And then there are administrative restrictions, you cannot buy a house in China and resell it at will. In addition, large currency reserves and a huge trade surplus defend the RMB from any other attempts to attack. All this effectively isolates Chinese finance from the world, so it is difficult for a Chinese financial crisis to spill over into the world.

In addition, the markets have understood that the Chinese business cycle is closely dependent on credit. On a 2/3 year interval, the Chinese economy faces structural bubbles, which usually occur when the Chinese credit impulse turns negative. This happened in 2014-2015 and subsequently in 2018, when Chinese markets suffered significantly due to a clearly negative credit impulse. For this reason, what can be called "Lehman cases" in China are punctually resolved by government intervention.

This does not mean that the Evergrande/China slowdown is without global repercussions or that it can be completely underestimated.

The global credit impulse has been (mainly) driven by China in recent years but currently, we see a very uniform decelerating impulse across jurisdictions. The interesting thing is that the impulse is now clearly negative (a contraction of credit on the second derivate) likely because of a voluntary drawdown on the revolving facilities that were widely utilized during Q2/Q3-2020. In other words, credit growth is slowing fast as 1) liquidity facilities are not as needed now and 2) the impulse from the fiscal and monetary side is weakening in YoY terms. Gravity pulls.

The big question is if this is something to worry about.

Thus, it is presumable that the Chinese authorities will place a limit on financial stress in the markets. Indeed, a systemic crisis that affects all investors can strongly influence capital flows and is therefore undesirable for a very open economy like China (see chart below).

In addition to a direct bailout intervention (in the case of Evergrande) more fiscal and monetary loosening can be expected. New targeted liquidity measures will help to ease the pressure on the sector and at the same time calm the markets. In the summer the PBOC reduced the reserve requirement for domestic banks and increased the share of loans to the real estate sector.

Now the key question is when the easing will take place.

In real estate, for example, contracted sales have peaked and home prices may be near a high.

Therefore, an intervention is more urgent than in the past three months, so loosening could occur in the next 3-6 months.

Where is China heading?

China's current financial landscape seems to be driven by a single motive: the policy change initiated by the CCP to curb leverage.

This structural change began some time ago. In terms of changes, mainly, it refers to the introduction of three red lines (as noted by one of the most relevant @FinTwitter):

Loan to asset < 70%

Net leverage < 100%

Cash to short term debt > 1

What is the rationale for these three key points?

First, it is to prevent the risk that a systemic crisis left unchecked could have brought down the entire financial sector. In hindsight, this was the right move, as the center of the possible systemic crisis to date is the real estate sector, which represents a significant slice of China's GDP with strong upstream and downstream linkages. However, for the real estate sector, high debt is not the only issue (which makes it clear why those 3 key points are not enough).

A common practice (understood as irregularity) for Chinese construction companies (a game at which Evergrande excelled), was to offer land at significantly higher than market prices (the risk was transferred to the apartment buyers and the banks that financed the purchase). That model worked well for local governments, banks, and families because home prices were rising. So much so that a serious affordability crisis has emerged in major cities over the past 15 years. And household debt has risen well above disposable income - below household debt as a % of GDP.

Hence, it wasn’t hard to figure out the economic disaster in the making: exponential price rises with explosive household and construction leverage. (For instance, It is estimated that China's real estate sector accounts for approximately 70% of Chinese household wealth vs. less than 30% in the US).

But that is not all...

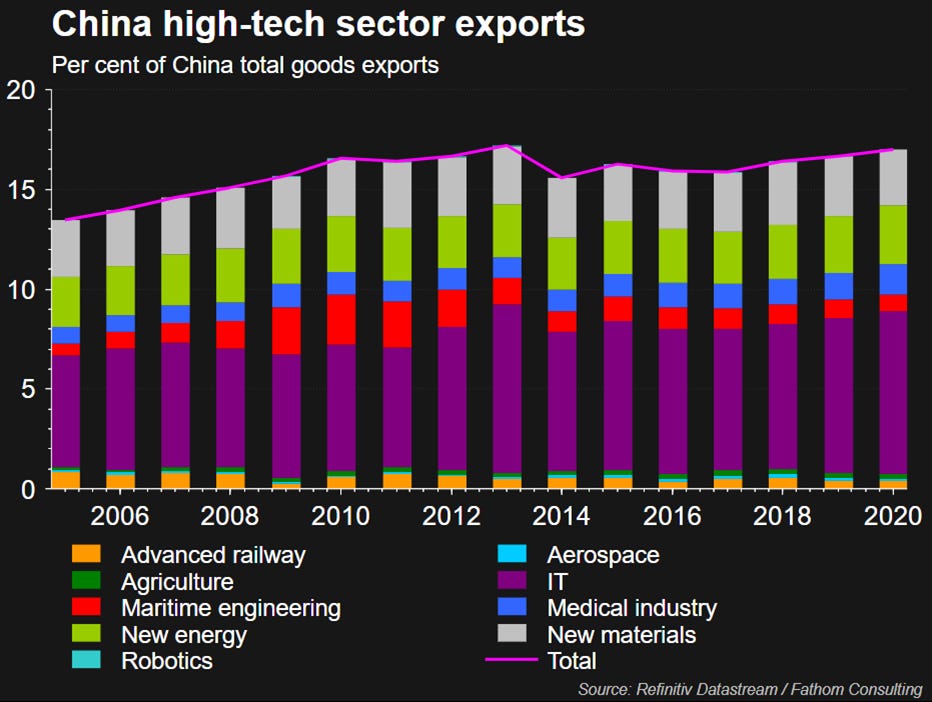

As a result of years of seeking easy growth in the construction industry through excessive use of leverage, the poor capital allocation has created a capital appetite in the most innovative and high-tech sectors (see chart), and that a headwind for a re-balancing towards a more consumption-driven growth was created.

At some point, reigning in lending to the real estate sector became vital to address the structural problem of misallocation of capital. This also explains the limits on venture capital investment in real estate and, more importantly, a curb on all the irregularities that have characterized that sector.

The issue of irregularities is at the heart of what is happening with Evergrande. So there is a new paradigm dictated by a set of economic realities that the CCP can no longer ignore and, more importantly, the CCP can loosen the rules a bit, but it cannot reverse course. China cannot allow consumers to go bankrupt or allow a rogue unproductive sector to expand further.

The tail risk from implementing this new paradigm must be objectively assessed. It is not necessary to look solely at Evergrande credit, but from a forward-looking perspective, the entire Chinese high yield market must also be measured in a short time. Indeed, the effects on individual bond issuers are not yet apparent (as reported above). However, the aggregate view on HY is starting to feel the symptoms.

Ultimately, the Evergrande story needs to be clear that in an economic model where growth is driven by businesses, a disproportionate level of private debt can have dangerous implications. However, if the relevant government is prepared to absorb the social costs, enterprises like Evergrande cannot be equated with the Lehman Brothers event. China's non-financial corporate debt is 165% of GDP compared to less than 100% in more developed markets.

Total debt is no higher than its counterparts in developed markets, but unlike those economies, it is concentrated in the private sector. High corporate debt is a legacy of the strong banks and real estate deregulation that accompanied the boom of the early 2000s. Corporate leverage displaces household debt, which is 20-30% lower in China than in mature markets and constrains monetary policy. Thus, corporate balance sheets are vulnerable to any "pro-consumer" changes by policymakers.

Key Takeaways

Evergrande's business model is broken. Under the new rules, Evergrande can no longer sell properties before it has formally finished building them, a system that is an important part of Evergrande's business model. In the past, the group had largely taken advantage of this model to finance itself and keep its operations afloat. So a significant contribution on this default comes from regulation. For this reason, one should be cautious about assumptions of a total bailout of Evergrande by the Chinese government.

It's much easier to contain Evergrande than Lehman, but that doesn't mean that Evergrande's explosion won't have repercussions - after all, it's still a $305 billion intervention.

Despite the fact that the news from the broader housing market is terrifying, the markets have been relatively slow to respond compared to what one might expect (the reaction on Monday, September 20th, should have come in the past few weeks). Why this? Because the markets are trying to decipher the intentions of the Chinese authorities. For years there has been an alarm in Chinese circles about the possibility of a Minsky moment, often expressed out loud. Officials know what could happen and are determined to prevent it if they can.

One thing is certain: Beijing will not bail out Evergrande tout court. In 2020, the Chinese government allowed several state-owned enterprises to go bankrupt, showing a change in mindset regarding defaults. In the past, it was assumed that the government would initiate a bailout if a state-owned enterprise failed. This year, the government has shown that it will only intervene if contagion risk is identified, such as what we witnessed this year with Huarong Asset Management.

A likely avenue for intervention by the authorities could be to encourage debt extensions, with a push on credit committees.

But to keep in mind is that if no signs of financial stress emerge in the immediate term, it is not advantageous to conclude that there will be no contagion.

Bonus Track

In the following scheme a reminder of the events relevant to Evergrande. Useful for reconstructing the history of default.

The Macro Code is an open diary on markets, macro-trends and structural changes.

To receive updates in newsletter format, follow the form below.

Please, note that The Macro Code represents personal views only.

Xi the Fool is attempting to forge a CCP-Xi fashioned capitalist-socialist (what's that???) economy; his assertiveness is like yelling out loud:" We the big-government are above markets laws, there's no invisible hand, the only hand in wich we believe is the one needed to promote a "common prosperity"; you tech/biz/whatever billionaires are subject to our own control; your behemoths companies have to align to our set ojectives otherwise you're gonna go destroyed".

All the above + social ranking + Great Firewall + latest attemp to impose max 3 hours of videogames play per week for kids sound very, very like Orwell'1984. Quite terrible, awful, unfair and to be fought.