The Macro Code #4: When inflation dreams become nightmares

Bottlenecks, supply-side squeezes and inflation perspectives

Welcome to The Macro Code, an open diary on markets, macro-trends and structural changes.

“All things are only transitory”.

Johann Wolfgang von Goethe

Will it be valid this time as well?

Things might get a bit bumpy for markets as the summer draws to an end and people return to their daily lives. In developed economies, most of the working-age population has been vaccinated, most social restrictions have been lifted and we are closer to normality in terms of working practices than we were in September of last year. However, the looming Delta variant continues to keep the spotlight on the metrics for assessing the evolution of the pandemic and put the effectiveness of vaccines at risk. This is contributing to ongoing disruption in global supply chains and labour markets. Structural demand is up, while supply struggles to keep pace.

This newsletter is divided into three sections.

First, we look at global inflation dynamics, detailing the causes of the supply squeeze on semiconductors, trying to identify what will be the persistent drivers of upward inflation in the medium term, once transitory effects such as bottlenecks have faded. Second, we look at the US context to understand the relationship between inflation, employment and the Fed's future monetary actions. Finally, we will examine what causes the current failure of the U.S. 10-year Treasury to rise compared to what occurred during the 2013 taper tantrum.

A global view on inflation

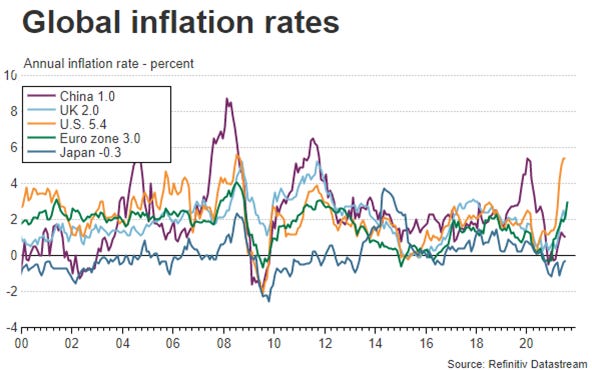

Core inflation is above historical averages. Headline inflation has risen globally and now stands at 5.2 in US, 2.0 in UK, 1.9 in Euro Area e 0.1 in Japan.

Transitional factors such as base effects and supply chain disruptions are contributing to this acceleration. Consequently, it is important to examine what factors during the post-pandemic recovery have created supply-side bottlenecks.

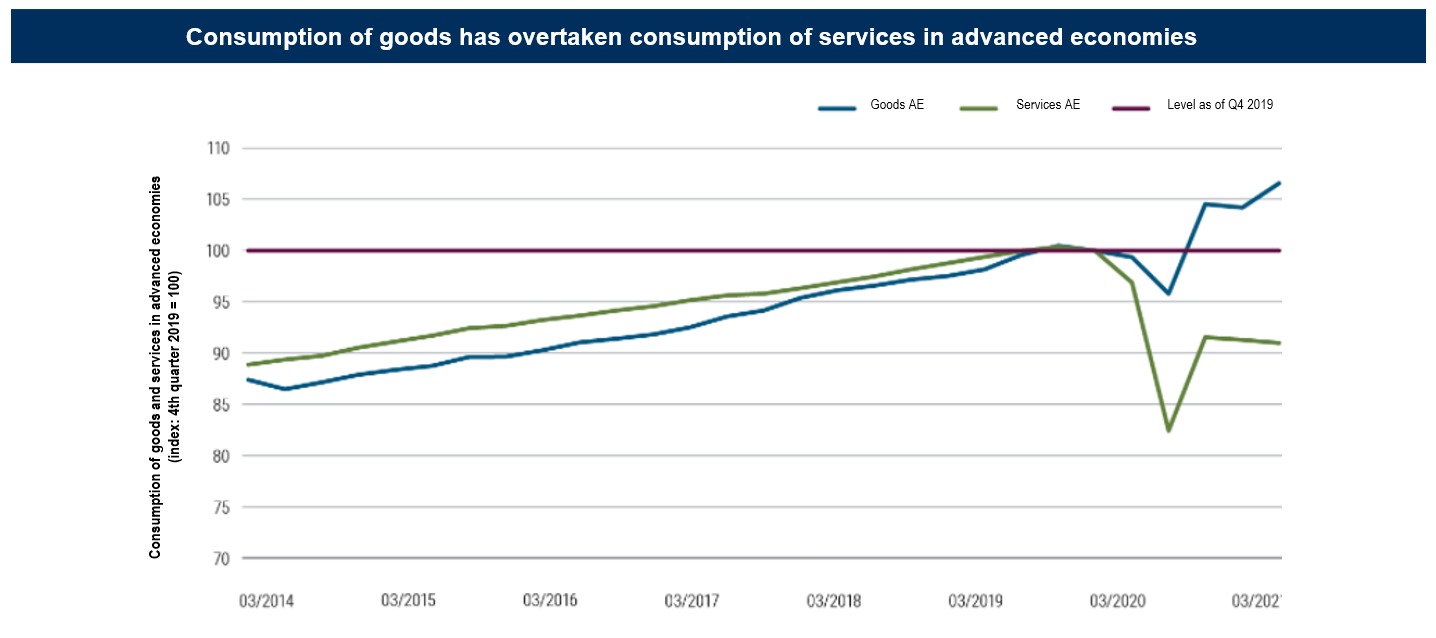

First, many aspects of the COVID-related recession were unprecedented, but the absence of contraction in consumer goods demand was especially so. In developed markets, consumers generally substituted purchases of services for purchases of durable goods. In the U.S., there was an explosion in exercise bike sales and gym memberships plummeted. Globally, there has been an acceleration in demand for automobiles and a decline in the use of public transportation.

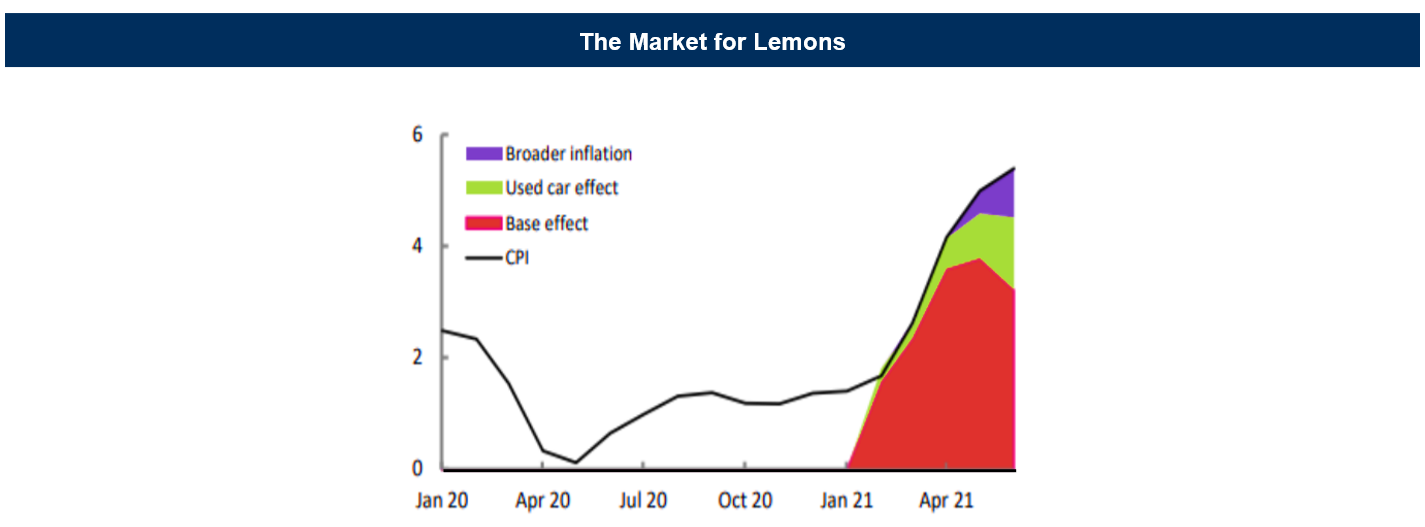

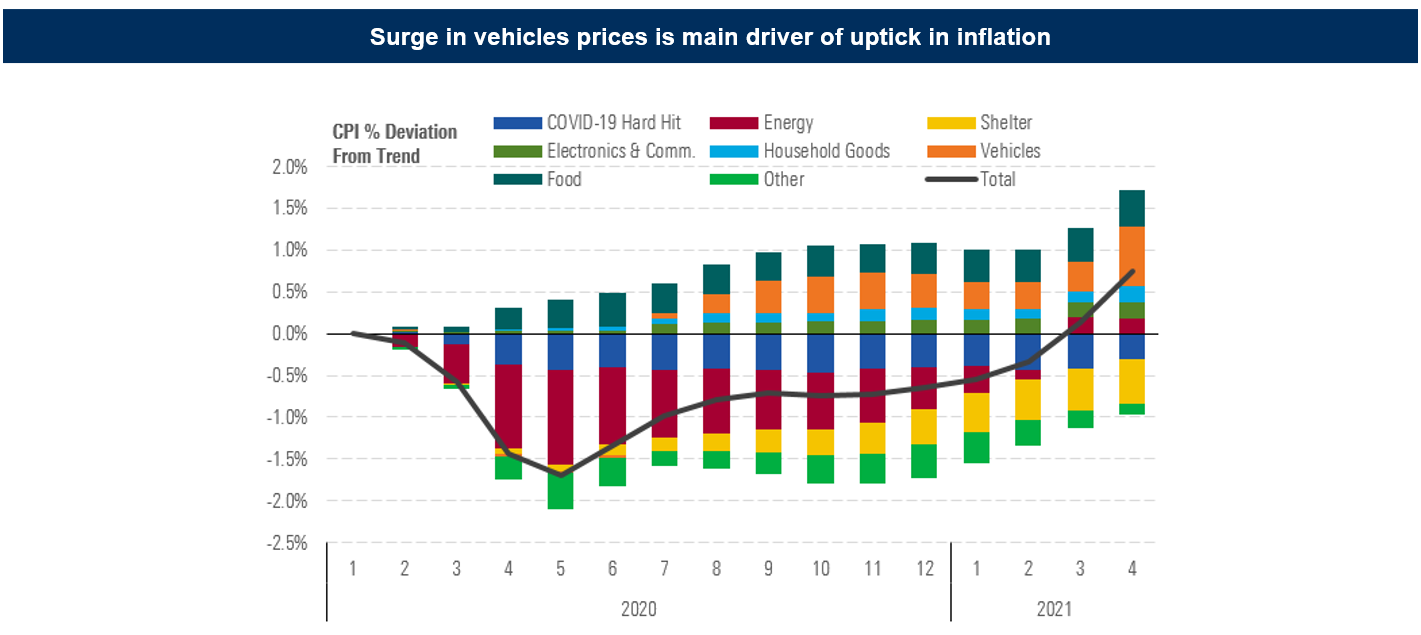

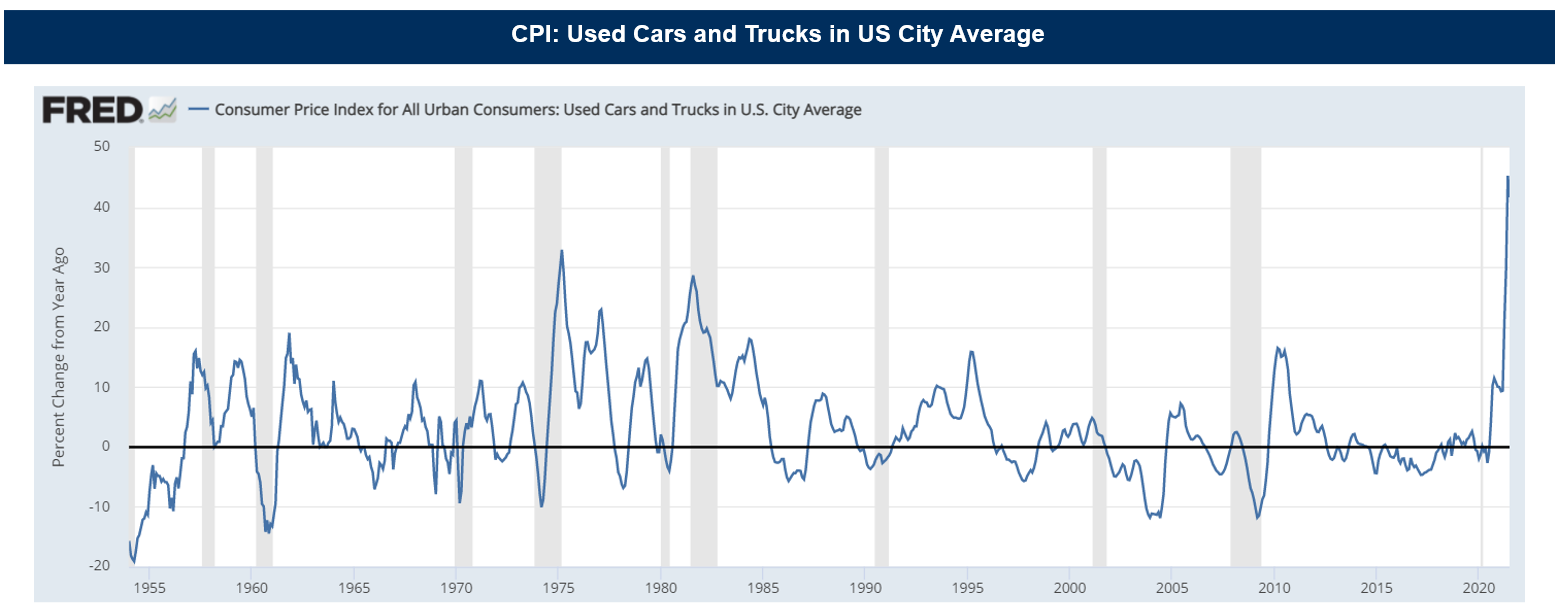

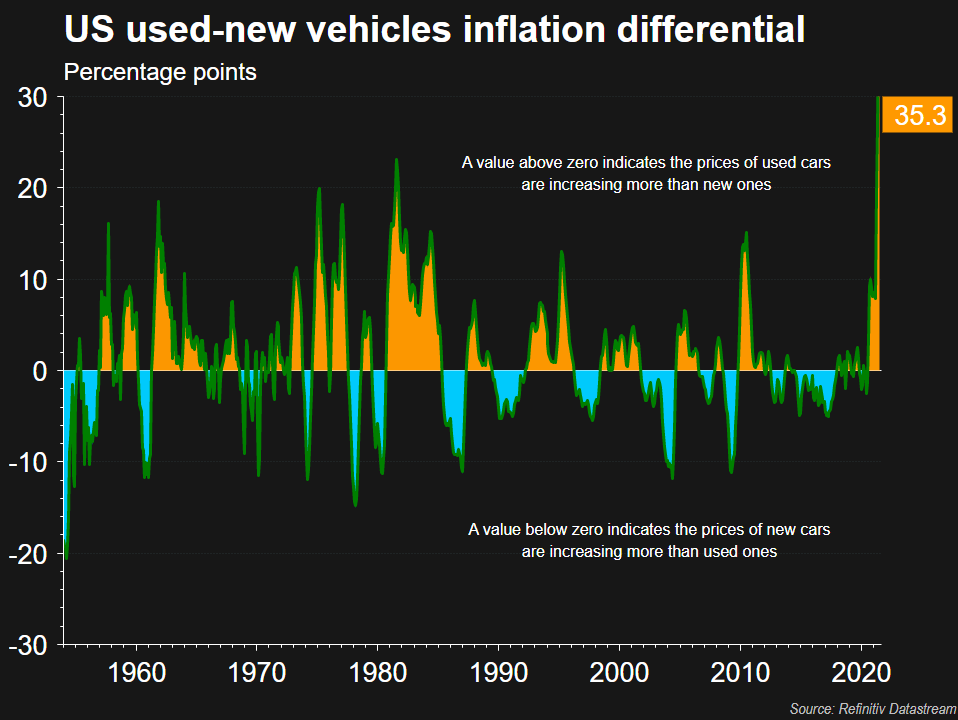

Looking closely at the data, we will note that the acceleration of asset price inflation in developed markets has been largely driven by skyrocketing prices of used cars in the United States. Indeed, the global shortage of semiconductors has hampered the production of new automobiles in the United States more than in other developed markets.

The price effects of commodity shortages are most evident in the second-hand car market in large part because U.S. car rental companies to rebuild their fleets after last year's liquidations have turned to the used car market.

However, as reported by a research study by the Cleveland Fed, these shortages and their effects on new car prices will subside within the next six to nine months.

What is the reason for the semiconductor shortage?

Early in the pandemic, the global transition to a remote lifestyle led to a sharp increase in demand for microchips, especially for consumer electronics. Subsequently, with large-scale vaccine distribution and gradual re-opening of advanced economies, economic recovery exceeded expectations, and durable goods such as automobiles and appliances experienced increased demand. Along with the surge in consumer demand came an excessive surge in demand for semiconductors, which were essential to continued production.

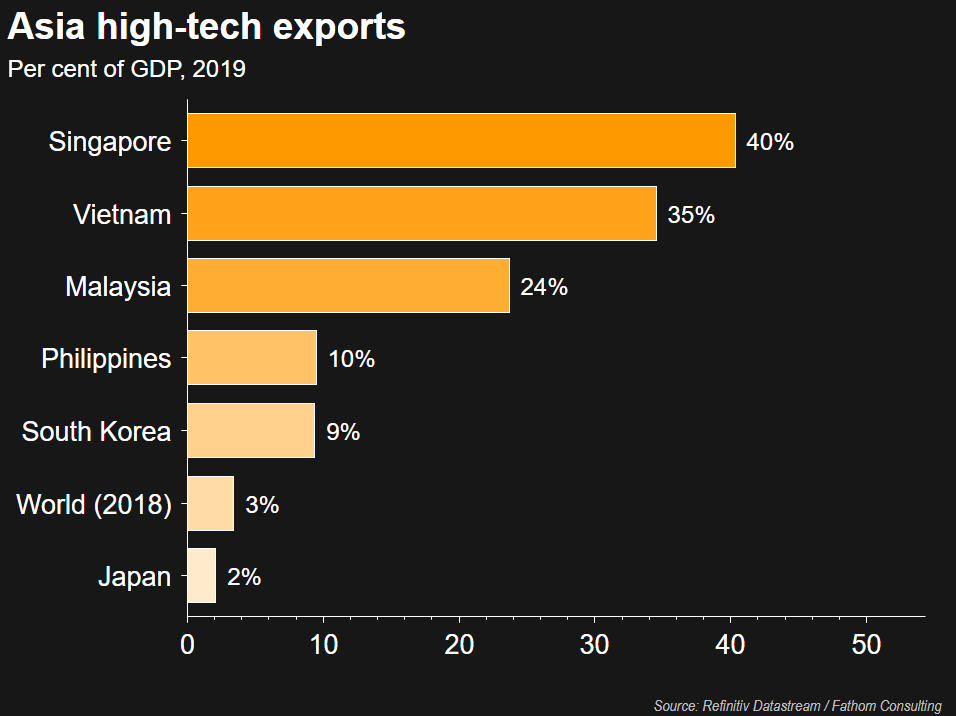

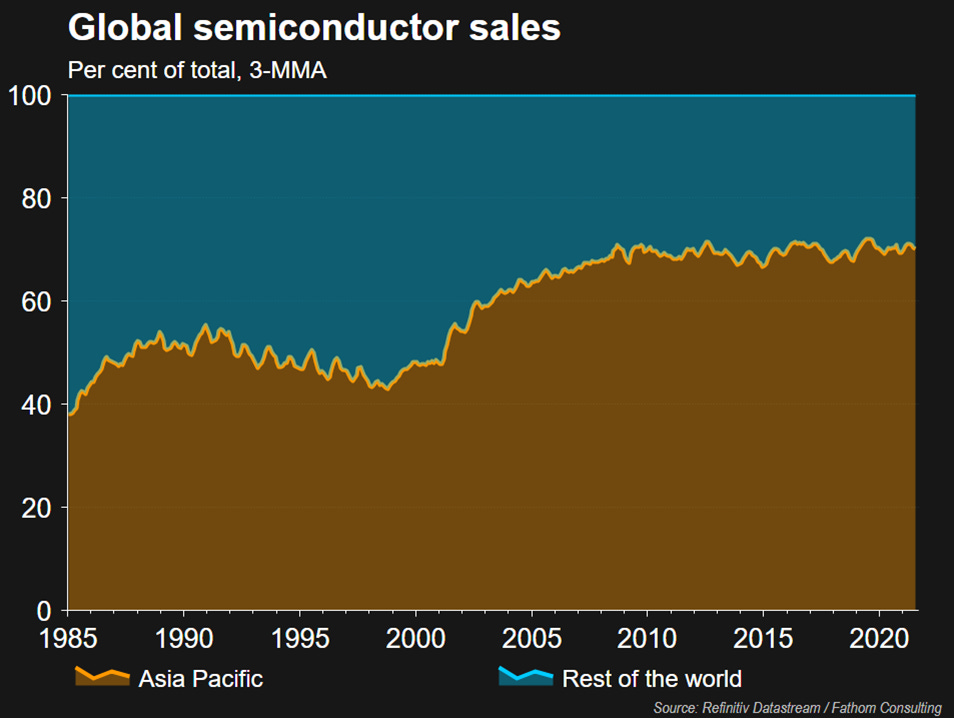

Production problems were exacerbated by a lack of geographic diversification among semiconductor manufacturers. Despite the global need for chips and chip-based products, the target industry is largely based in Asian countries.

Limited chip supply and unbalanced market share made supply chain disruption inevitable.

Moreover, most of microchips production is destined for China, which — despite its goal to expand its technological manufacturing capabilities, as part of its Made In China 2025 plan — remains dependent on imported semiconductors

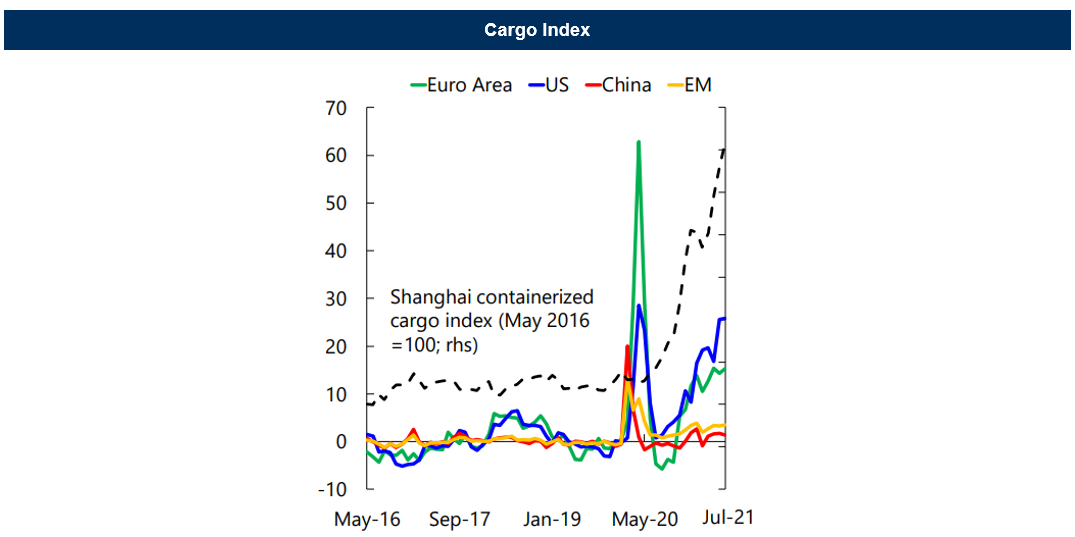

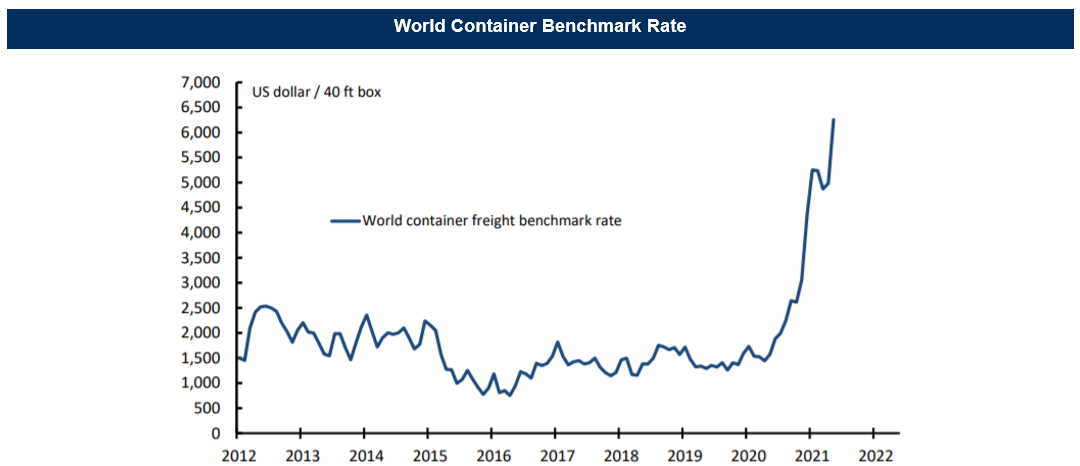

However, bottlenecks have not only occurred on the supply side of semiconductors. There have also been obvious issues in the machinery of global trade, with the creation of a boom in the container market with no sign of abatement in the near term. For instance, the continued easing of lockdown restrictions across the globe, combined with the capacity constraints in other sectors, means that charter hire rates for the multipurpose and heavy-lift fleet are expected to continue to rise from their current peak for the remainder of the year, according to Drewry’s Multipurpose Shipping Forecaster.

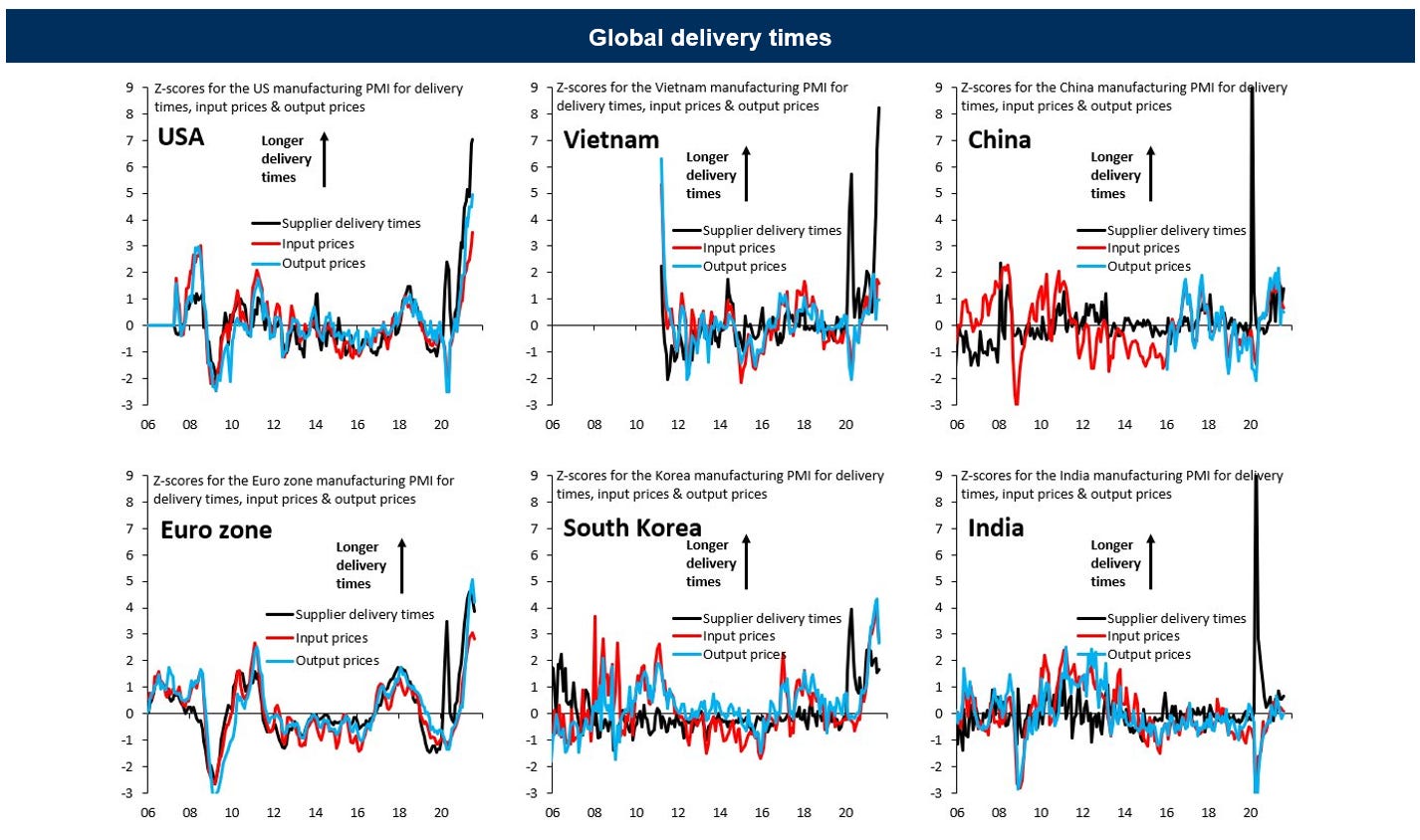

Looking at the short term, these deep disruptions in global supply chains have a direct effect on delivery times. During August 2021, Vietnam saw a sharp worsening in delivery delays (top middle), but this is strictly related to the COVID delta outbreak in Vietnam and not to the rest of Asia, where delivery delays are modest. However, the US (top left) remains the key global outlier in terms of delays and output price mark-ups.

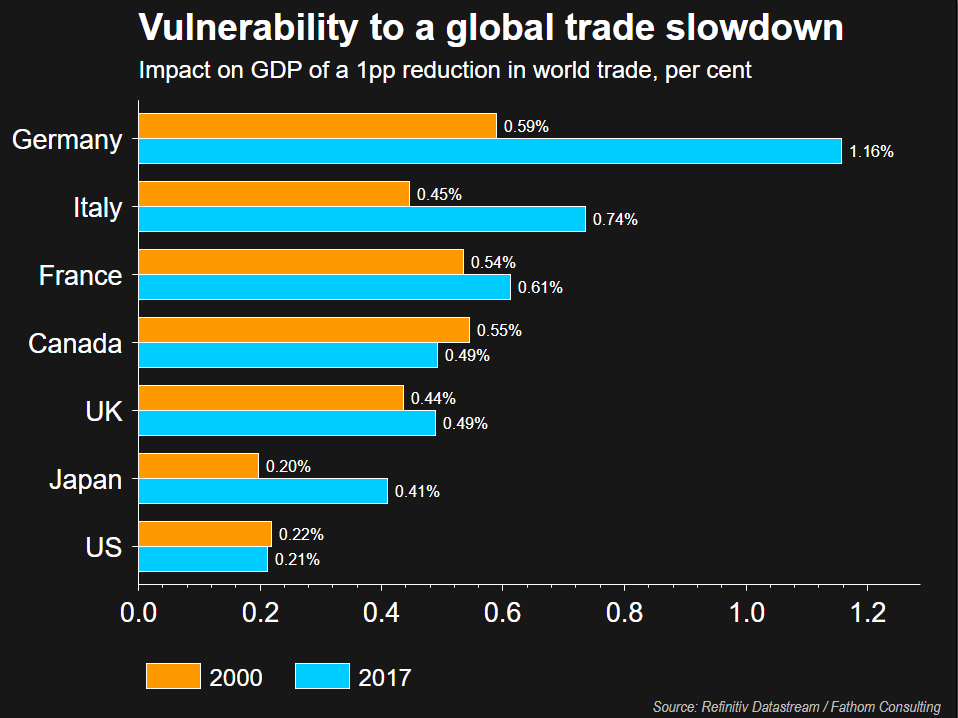

Looking at the long term, on the other hand, European countries appear to be the most damaged by a potential slowdown in trade, since the re-establishment of trade contacts is more difficult in those economies that have highly fragmented supply chains (and European countries present this characteristic).

Despite these supply-side slowdown factors, most economic forecasts expect these constraints to ease in 2022.

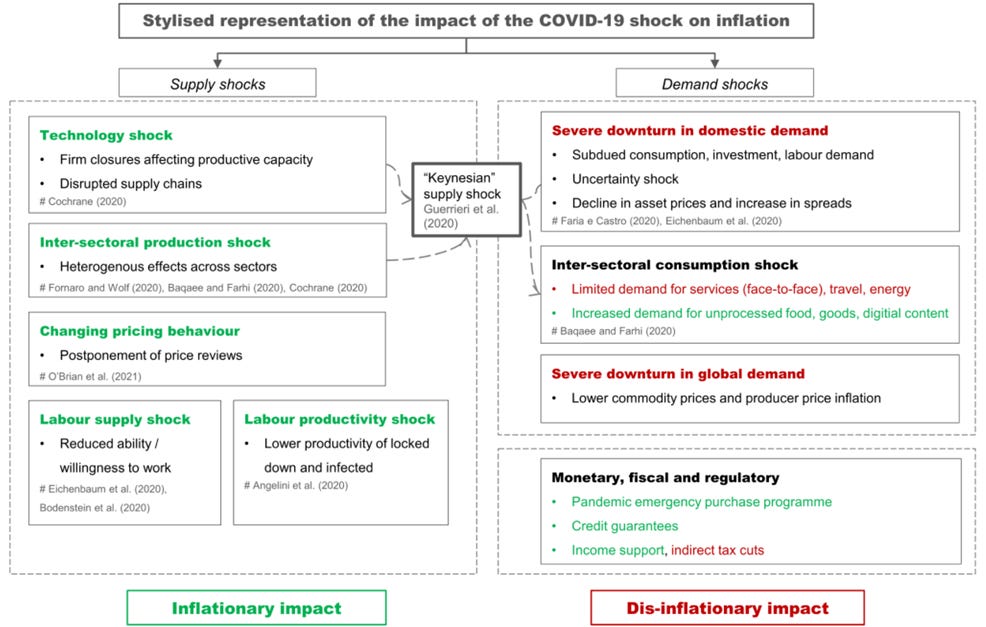

Ultimately, the effects of the Covid-19 shock on the supply and demand components have become more complicated, intertwined and amplified over time. The constellation of shocks hitting the economy is changing as the recovery progresses. Pricing inflation during a period of shocks that start from the supply side and spill over into the demand side is difficult for both policymakers and investors.

The key message here is that once transitory effects (such as precisely base effects and supply chain disruptions) cease to exist as capacity is gradually reached, there may still remain persistent drivers of higher inflation over the medium term.

1. Real wage growth lags

QE has fueled inflation in asset prices, but real wages have been eroded or have barely increased in advanced economies. However, during the summer of 2021 wages rose, with growth above pre-pandemic levels in the U.S. and Europe

2. Commodity prices

Commodity prices nearly doubled in 2020. From a geopolitical perspective, this increase reflects a shift in purchases away from China and toward the US. The strong US demand for commodities is driven by the implementation of the infrastructure plan undertaken by the Biden Administration and the management of the green transition (see here).

3. Asymmetric energy transition

Coal and gas prices have risen dramatically. In addition to the restart, a number of weather and geopolitical factors have constrained coal and renewable energy supplies. It has been difficult to bring other energy sources online. This is putting significant pressure on the prices of available energy sources.

An orderly, albeit unbalanced, transition to a net-zero emission economy could have obstacles along the way that could lead to higher inflation. Why?

Just think of the rising prices of metals and minerals such as copper, aluminum and lithium that are essential to solar and wind power, electric cars and other renewable technologies.

Two of the most important metals for green electrification are copper and aluminum. But investments in these metals have been depressed by companies to comply with ESG criteria. However, the bottom line is that the world needs more copper to stop global warming. Aluminum is one of the dirtiest metals to produce, but it's also one of the vital metals for solar power generation and other green energy projects, and according to the World Bank, it's set to face a particularly strong increase in demand in the coming decades (see here).

4. Supply Chain Onshoring

As reported earlier, the global chip shortage has helped exacerbate inflationary pressures. While this shortage can be described as transitory and prices will likely normalize in the coming year (see here), the shortage has highlighted the risks of global supply chain offshoring. It makes sense to think about greater onshoring of supply chains (see here) around strategic productions, both as per lessons learned from the pandemic event and as a way to protect intellectual property in a context of increasing geopolitical risk (see here)

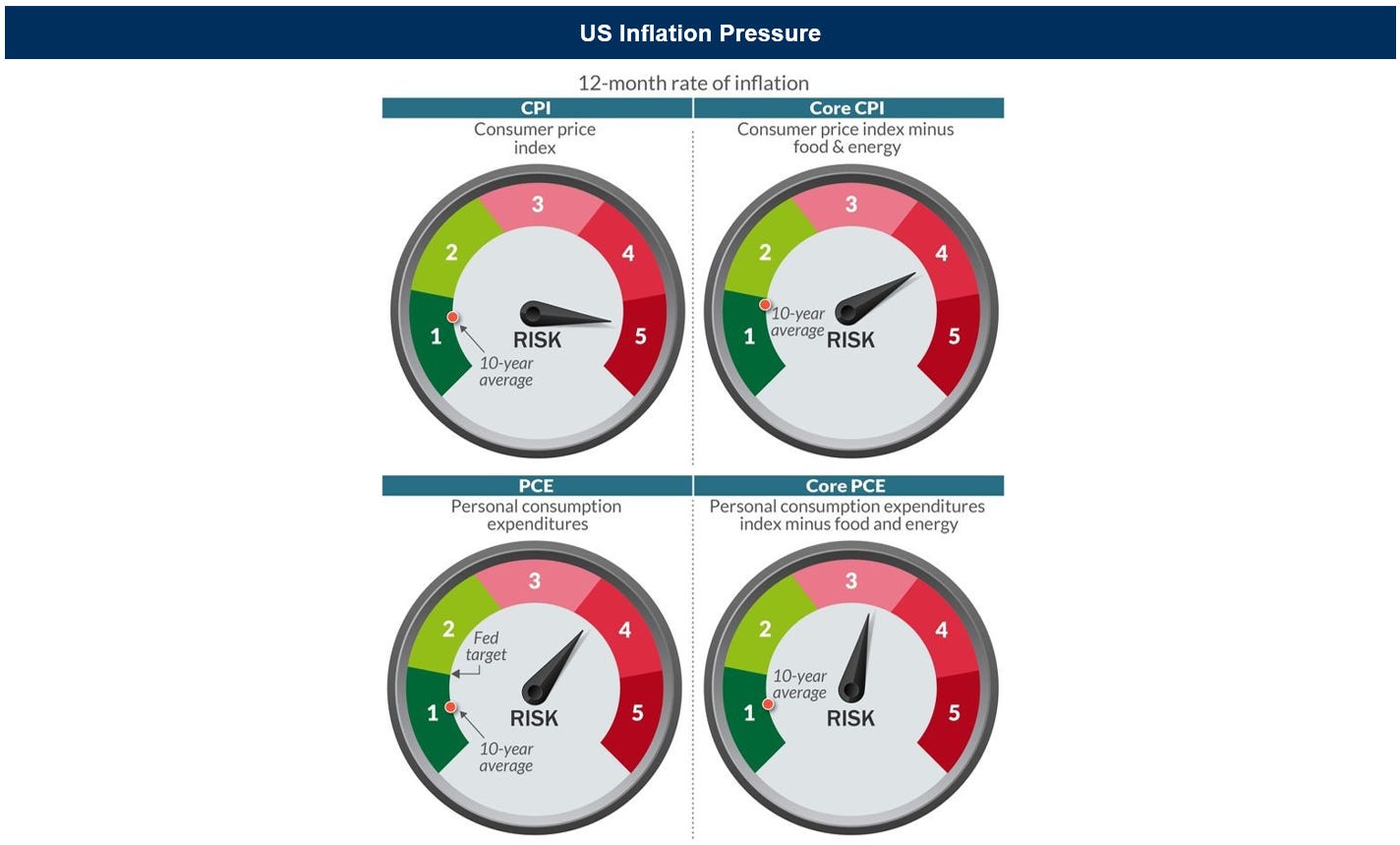

US Inflation perspectives

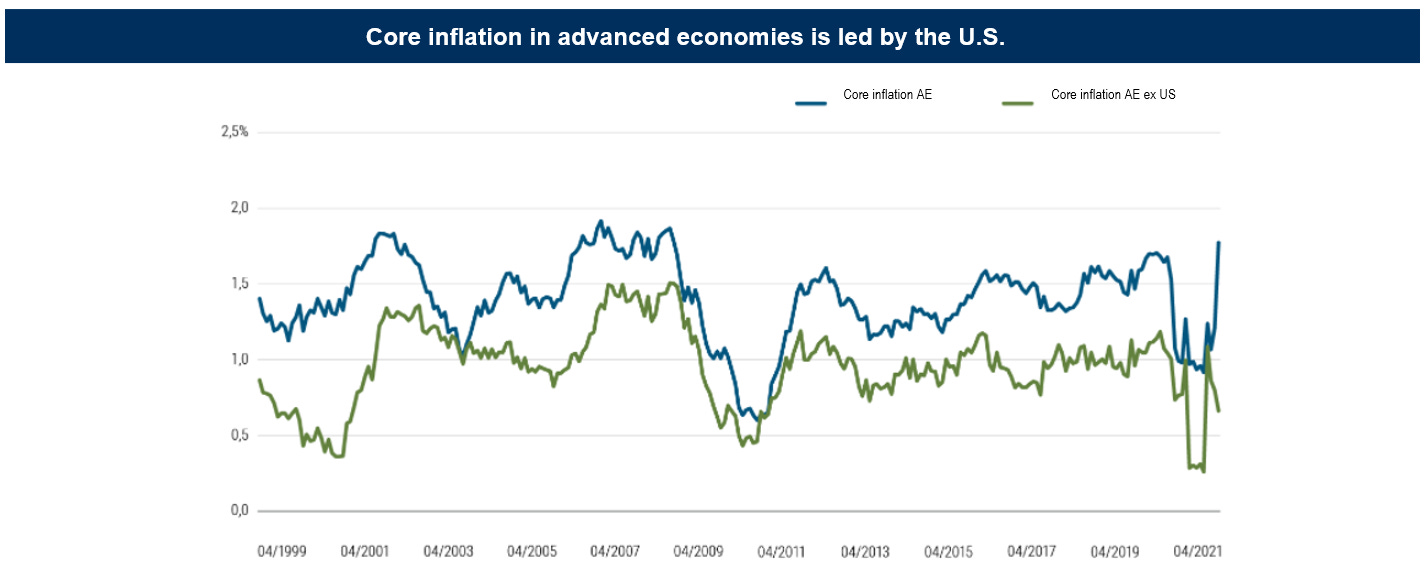

If we talk about inflation, surely it is necessary to start with the US. Why? Because core inflation in developed markets is primarily driven by US inflation. For example, as of April 2021, core inflation in developed markets outside the U.S. was around 0.6% year-over-year versus 3.0% in the U.S. This divergence occurred despite the global nature of bottlenecks in supply chains because demand for goods supported by fiscal stimulus in the United States was higher than in other developed markets.

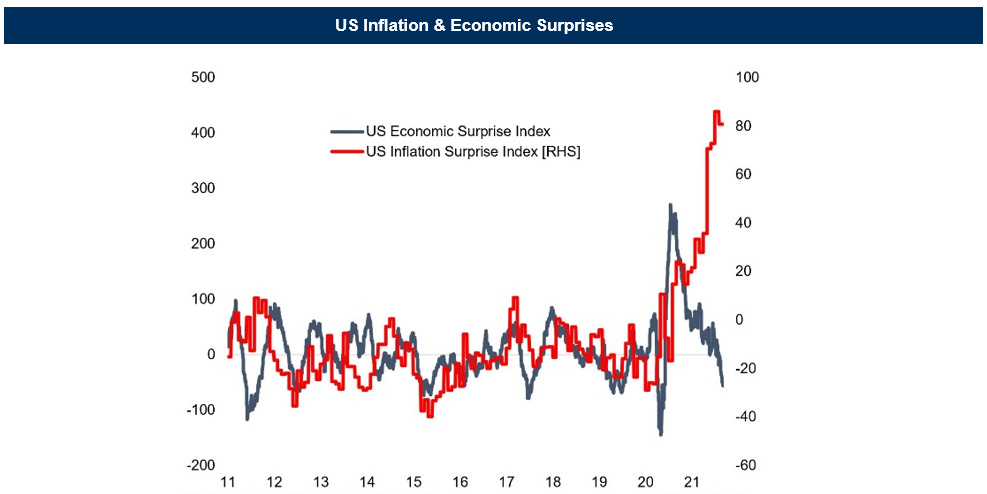

The central issue for markets is how long inflation will continue its upward trend. Inflation is by definition "transitory." What should be discussed is the length of the transience.

What emerged from Powell's speech at the Jackson Hole symposium in late August was that (1) much of the recent increase in inflation is relative prices not pure inflation, (2) these price changes seem temporary, (3) there is no pick up in wages so far, (5) global forces are favorable.

However, the markets remained skeptical about the slight hints towards Fed tapering. There are two points to consider.

First, the Fed wants to make sure labour markets and employment/participation rate recover. The risk of tapering too early amid a slowdown due to covid/delta is too high.

However, it is not clear why the stimulus should remain on. High unemployment rates around weaker states and minorities are microeconomic issues: monetary policy's one-size-fits-all hammer is not the right fix. Investment in education / re-training / tax redistribution are the key.

Second, the expiry of Powell's mandate must be considered, for now, he is personally incentivized to not rock the boat until his re-appointment. (He will be reappointed - the current administration would like a new candidate. But keeping Powell leaves a free option to blame the previous administration, should inflation remain high). This second factor also had a direct effect on the Fed Chairman's process of anchoring inflation expectations in his Jackson Hole speech. Powell started with “as long as longer-term inflation expectations remain anchored” we'll be fine. But he did not specify what the Fed will be willing to do to anchor expectations. It should have anchored expectations to clear policy choices, since they are not determined by some exogenous force.

No taper tantrum this time?

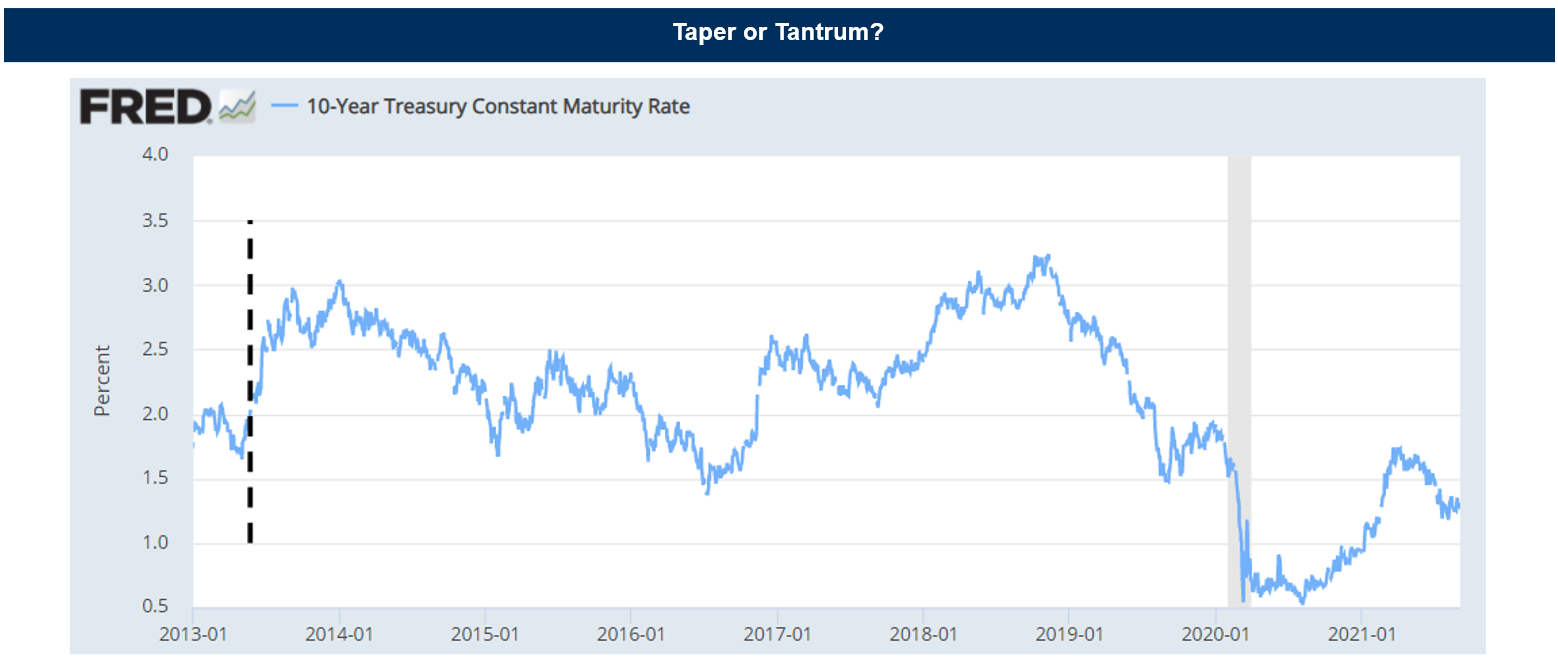

In the chart below we can see the daily yield on 10-year U.S. Treasuries since the beginning of 2013. On May 22, 2013, Federal Reserve Chair Ben Bernanke announced that the Fed would start tapering asset purchases at some future date, which sent a negative shock to the market, causing bond investors to start selling their bonds. As a result, the yield on 10-year U.S. Treasuries rose from around 2% in May 2013 to around 3% in December. This sharp climb in yields is often referred to as the “taper tantrum.”

In late July 2021, Federal Reserve officials signaled that the Fed would start reducing the volume of its bond purchases later in the year. This signal made some investors worry about another taper tantrum; however, it might not be the case this time.

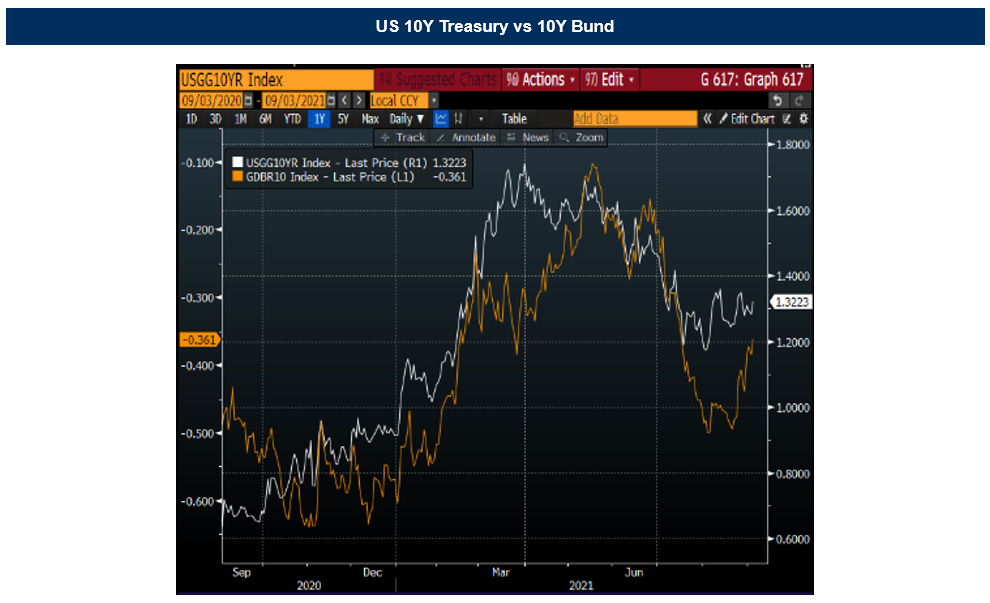

The Fed's current dovish attitude in undertaking tapering has resulted in a fall in the 10-year Treasury Yield. Despite the efforts of many analysts, it is difficult to understand this price action in the US. For example, if we look at the Eurozone, the 10-year German Bund Yield has been rising sharply since the markets focused on ECB tapering.

However, this current failure of the 10-year Treasury to rise compared to what occurred in the 2013 taper tantrum could be related to a few structural factors.

Presence of the Delta variant.

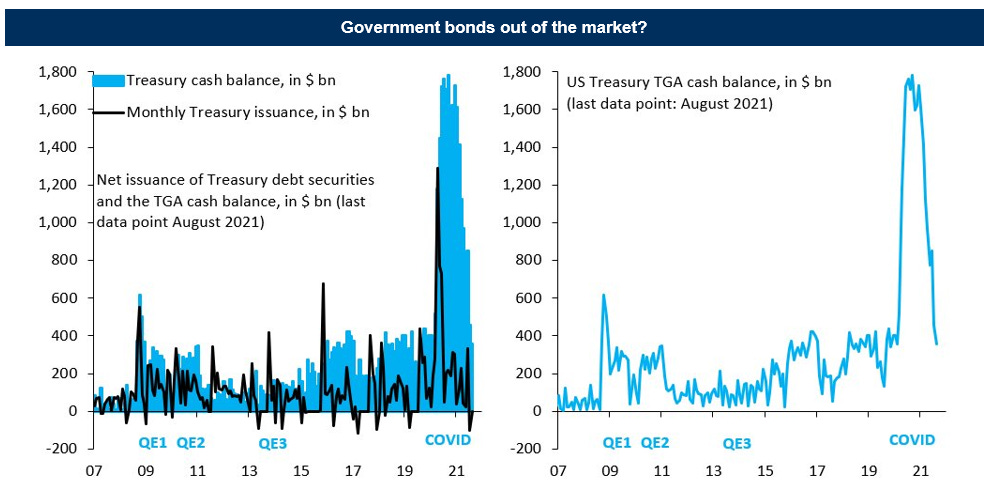

Unlike 2013, when Bernanke repeatedly said that yields were too low and needed to rise, the Fed now has a much more cautious stance in the tapering process (the announcement in 2021 was in line with market expectations and the announcement in 2013 came earlier than expected). More importantly, we need to consider that August was another month where net debt issuance was slightly negative (left chart, black line). Thus, once the Fed's QE was added at a steady $80 billion pace, the public sector (Treasuries + Fed) again took government bonds out of the market, putting pressure on yields.

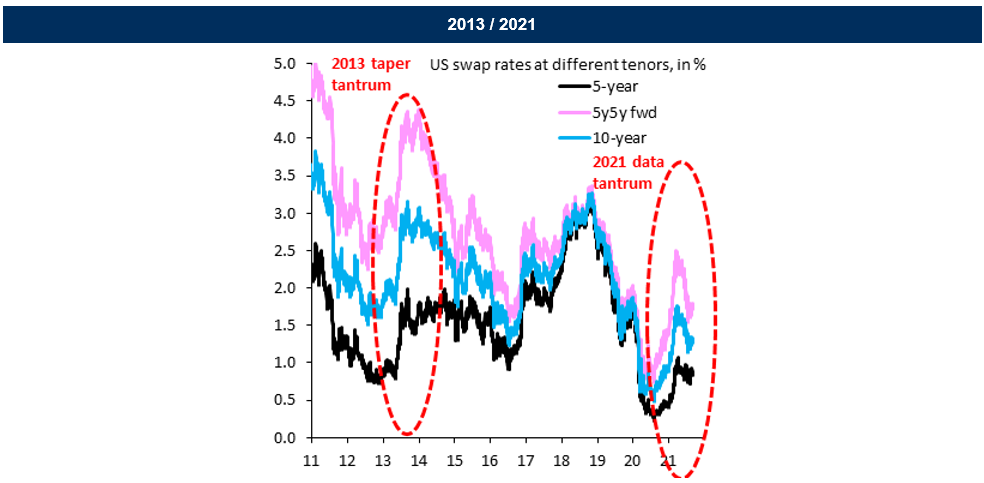

Changing perspective but remaining on the same metric, we can note that the puzzle about the fall in 10-year yield (blue) since April is driven entirely by 5-year yield 5 years forward (pink). Why would those things weigh on 5-year forward yield? The enigma is yet to be discovered. That's hard to reconcile with anything going on now, whether Fed tapering or the Delta wave. For instance, there's a well-known puzzle in finance that 5y5y forward breakeven inflation is highly correlated with swings in oil prices today. Finding an explanation for these effects proves to be difficult.

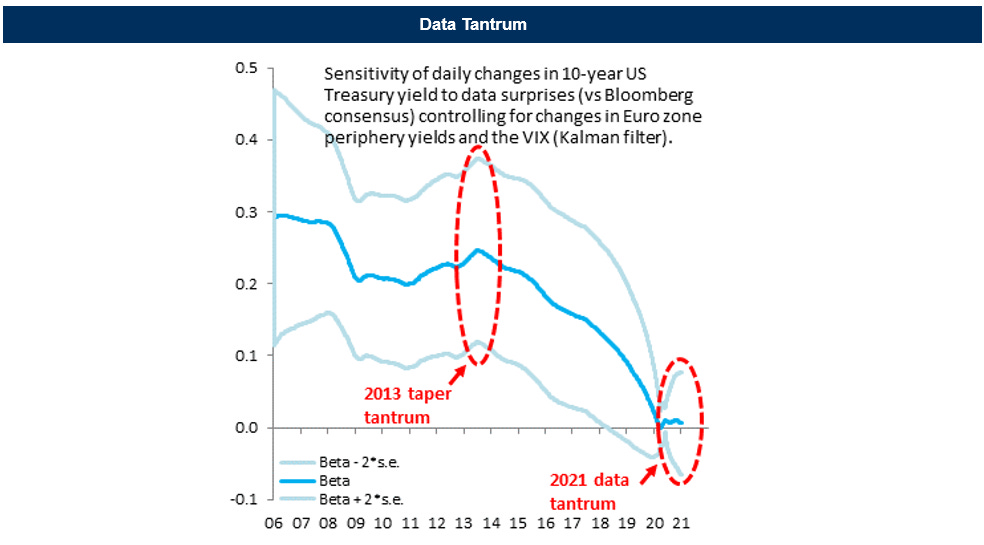

During these times sensitive to macro variables, markets have done the only sensible thing: they're completely ignoring data, with the beta of daily 10-year Treasury yield changes to data surprises = 0 (blue). This has never happened before and... the enigma becomes more complicated.

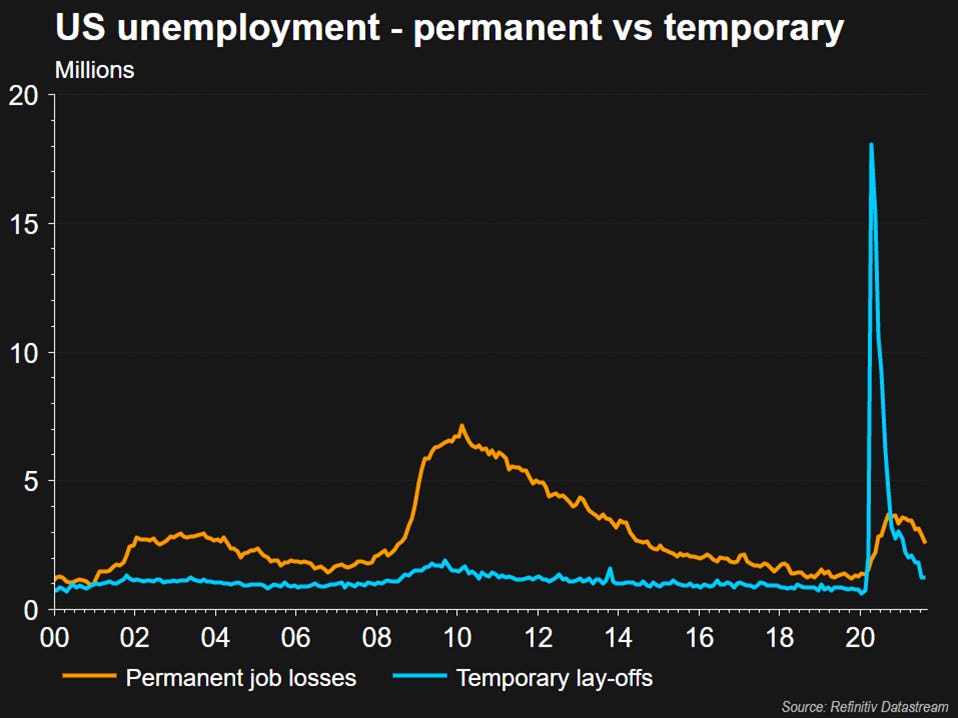

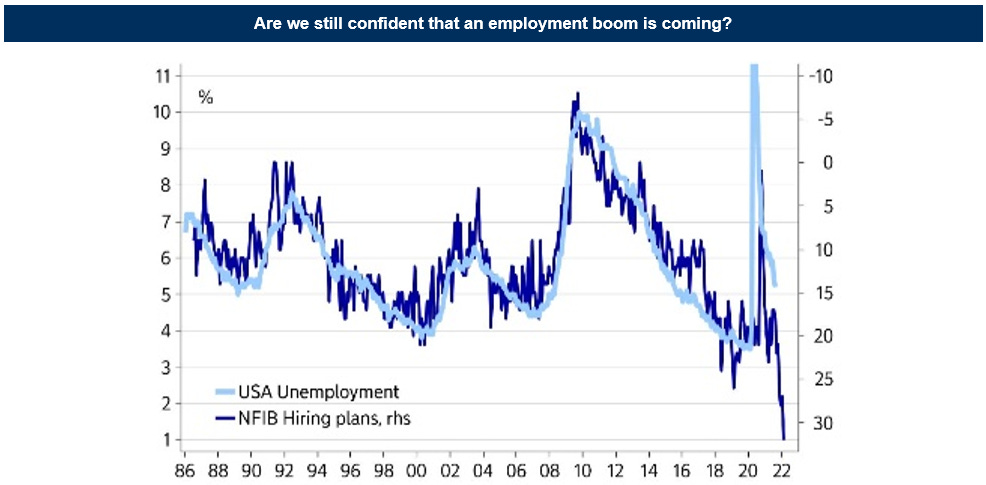

Moving forward, there is another element that impacts the tapering process. In fact, according to the latest data from the Bureau of Labor Statistics, the U.S. economy created 235,000 jobs in August, a sharp decline from the previous month.

Thus, U.S. job growth has slowed sharply as the Delta variant hits the recovery. The sharp slowdown in US jobs growth precludes the possibility that the Federal Reserve will announce plans this month to begin scaling back its pandemic-era stimulus. Are we still confident that an employment boom is coming? Probably yes. Hiring plans remain bullish. However, due to the spread of the Delta variant, there is a lack of labor market mobility that prevents plans from turning into hires.

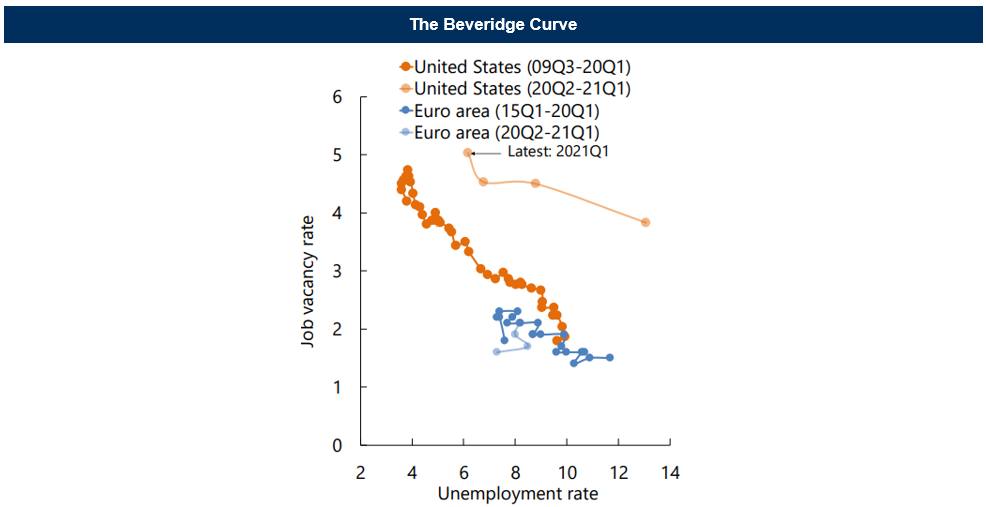

Meanwhile, the U.S. economy seems to be stuck in text-book stagnation.

The Macro Code is an open diary on markets, macro-trends and structural changes.

To receive updates in newsletter format, follow the form below.

Please, note that The Macro Code represents personal views only.