The Macro Code #1 - Getting ready for Jackson Hole

What are the global factors that may impact inflation dynamics in US, EZ, China and Japan?

Welcome to The Macro Code, an open diary on markets, macro-trends and structural changes.

"The world has largely exhausted the scope for central bank improvisation as a growth strategy"

Larry Summers

Today, Thursday Aug. 26, begins the Jackson Hole Economic Symposium organized as tradition dictates by the Kansas City Fed. The title of the 2021 edition is Macroeconomic Policy in an Uneven Economy, but the big question for which the markets are waiting for an answer is that of the taper time.

In this newsletter, we are going to analyze the global factors that may impact the timing of interest rate hikes by the central banks of the top 4 economies in the world according to nominal GDP figures: namely US, Eurozone, China and Japan.

Spoiler: In this update, we will only consider the outlook for inflationary trends in the four economies under review. We will not refer to possible monetary policy strategies. The objective of this note is to prepare for a better understanding of the global inflation environment on which this edition of the Jackson Hole Symposium is based.

As an opening consideration, we can say that according to the markets we are about to see the peak of the so-called base effects from raw materials in the coming months, after which inflation rates should begin to fall towards the terminal level that in the United States seems to be around 2.3%. However, this belief could be betrayed by two additional observations related to the current scenario:

The period of inflation above the 2% inflation target appears to be longer than central banks had anticipated at the beginning of the year.

If the dampening of the base effect does not have the expected effect on the reduction of inflation, the markets will revise the inflation estimates in a more structural phase.

In the following sections, we will look separately at the components that impact inflation in each of the four countries.

US

What are the factors to monitor in the US market?

According to Reuters, the Fed is expected to outline taper plans in September but markets are hoping for signals from Powell at the annual research conference on the trajectory of the $120 billion-a-month asset purchase program. The consensus among policymakers is not yet unanimous. Nonetheless, the call over when to raise interest rates from near zero remains, in all likelihood, far down the road. Indeed, the prospect of stimulus being reduced when the spread of the Delta-Covid19 variant and supply chain issues loom over a recovery that has started to look tired has spooked markets.

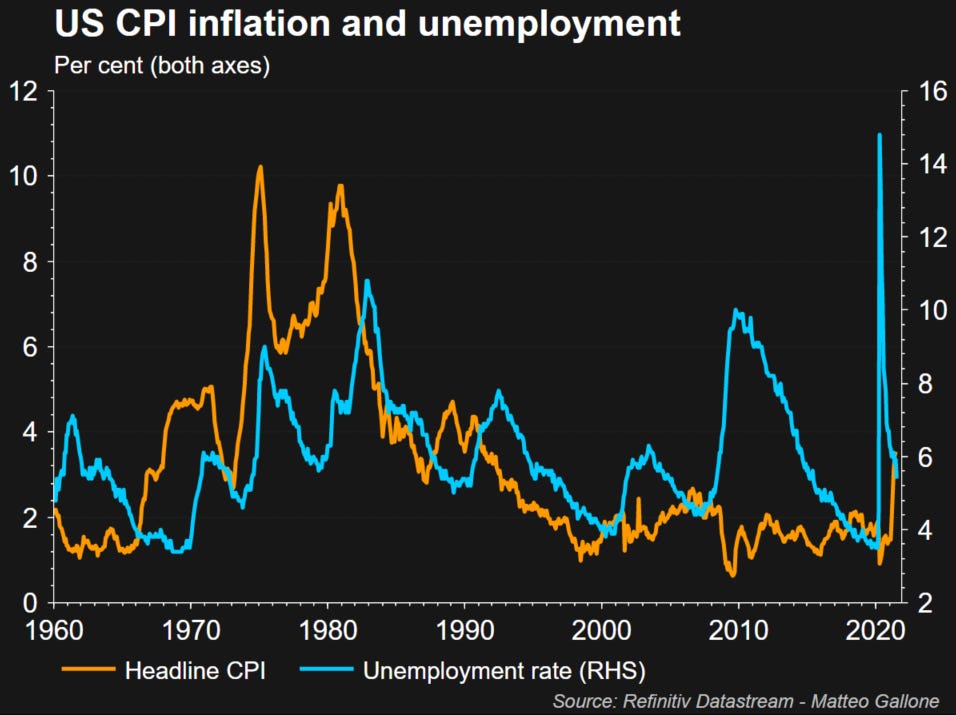

Despite a still divergent consensus, the most astute observers will have realized that the current scenario is changing. The excessive inflationary push is lasting longer than expected. As a result, the tone of Fed officials has changed. Moreover, some are lowering expectations of a full rebound to the pre-pandemic level of jobs or labor force participation. Since the Fed set a 2% inflation rate target in 2012, the pace of price hikes has generally been below that. It has now pledged to lift inflation on average by letting it run higher for a while. The details have not been specified. On a 12 month basis, high inflation this year has pulled the average up to target.

Concerns about the current warming of the economy are contributing to put pressure on central banks and markets.

Recently, Adam Posen, president of the Peterson institute for International Economics, expressed his concern about U.S. inflation: "I worry that inflation is a problem in the United States because of a collapse in fiscal credibility" (see here).

Along the same lines is Larry Summers, who says he is concerned that in the face of a sharp acceleration in inflation and generalized supply shortages, despite the sharp increase in money supply growth, the Fed continues its large-scale asset purchase program, keeping the Fed funds rate exceptionally low, in the range of 0.05-0.1%, both in absolute terms and compared to similar periods in recent history (see here).

Under the Taylor Rule, with actual inflation at 4%, target inflation at 2%, a gap between actual and potential GDP estimated at -2%, and an equilibrium interest rate estimated at 1%, we get a fed funds rate at 5%.

If 4% inflation were temporary and dropped to 2% already next year, at that point production would have reached its potential and the fed funds rate should be at 3%. These calculations are consistent with the average targeting suggested this summer and with the equilibrium rate at 1% instead of the previous 2%, in which case the policy rate should rise further.

Defenders of the Fed's current stance point out that long-dated rates remain very low, well below those suggested by the Taylor rule, so if markets are rational, monetary policy is consistent with these rates.

The trouble with this pattern is that long maturity rates so low are most likely caused by the Fed's willingness to hold them at this level.

Despite this, the Fed with its new regime of average inflation targeting is committed to not nipping job growth in the bud. In fact, under the traditional theoretical scheme, when inflation becomes too high, the central bank can tame it through rate increases, even if it comes at the cost of higher unemployment. When inflation is weak or unemployment high, the central bank can lower rates and trade more jobs for higher prices. However, in the 10 years of economic expansion since the GFC, that pattern has not worked. When unemployment fell, inflation remained muted, and Fed officials concluded that they could exploit it and take more inflation risk to create the kind of "hot" economy and robust labor market that helps the less wealthy. Problems, however, arose in the post-pandemic environment. Covid19 resuscitated what the Fed thought had escaped: conflict between inflation and employment.

In the midst of the debate over the new monetary policy framework in 2019, the Fed saw ample jobs and low inflation; now inflation is high, but with 6 million fewer people working than before the pandemic.

This has forced an earlier-than-expected reckoning on the problems left unresolved in the new strategy.

In US let's talk less about inflation and more about employment, please.

Eurozone

What are the factors to monitor in the EZ market?

Inflation in the Eurozone is more moderate than in the US market, so political pressure on taper time has little relevance.

In addition, the weak labor market and the Eurozone economy that will only return to pre-crisis levels by mid-2022 are strong arguments against any significant wage growth. We also point out that prior to the Covid19 crisis, when unemployment rates in many eurozone countries were at historic lows, wage growth in the eurozone only reached around 2.5%.

Therefore, with headline inflation expected to come in at 1.4% in 2023, the ECB clearly belongs in the club of hardcore “transitorians”.

The European market benefits from this scenario. The last months have been positive for European equities (since March 2020, they've climbed more than 70%). European PMIs rose to a 20-year high and inflation-adjusted bond yields are at record lows.

But not all is rosy. There are headwinds in the form of rising prices, supply chain issues, labour shortages and the Delta variant.

Additionally, the macroeconomic debate over the past week has been focusing on the fiscal space and how an eventual US tapering might affect the ECB's strategy. IIF reports that (see here) the US maintained market access during COVID, with the Fed's QE absorbing only 50% of the 2020 debt issuance (see the red segments in the chart below on the left). In contrast, in the Eurozone and Italy especially, relied almost exclusively on ECB QE (see total coverage in blue in the chart below on the right), so essentially no market access in 2020.

As a result, low bond yields in the Eurozone periphery do not signal ample room for fiscal maneuver. The ECB's QE is almost entirely covering deficit financing. Therefore, when we talk about taper time in the Eurozone, it is better to think from the perspective of peripheral yields, because even the slightest possibility of a reduction in ECB QE can cause yields to rise dramatically (see chart below).

Keeping calm in the Eurozone.

China

What are the factors to monitor in the Chinese market?

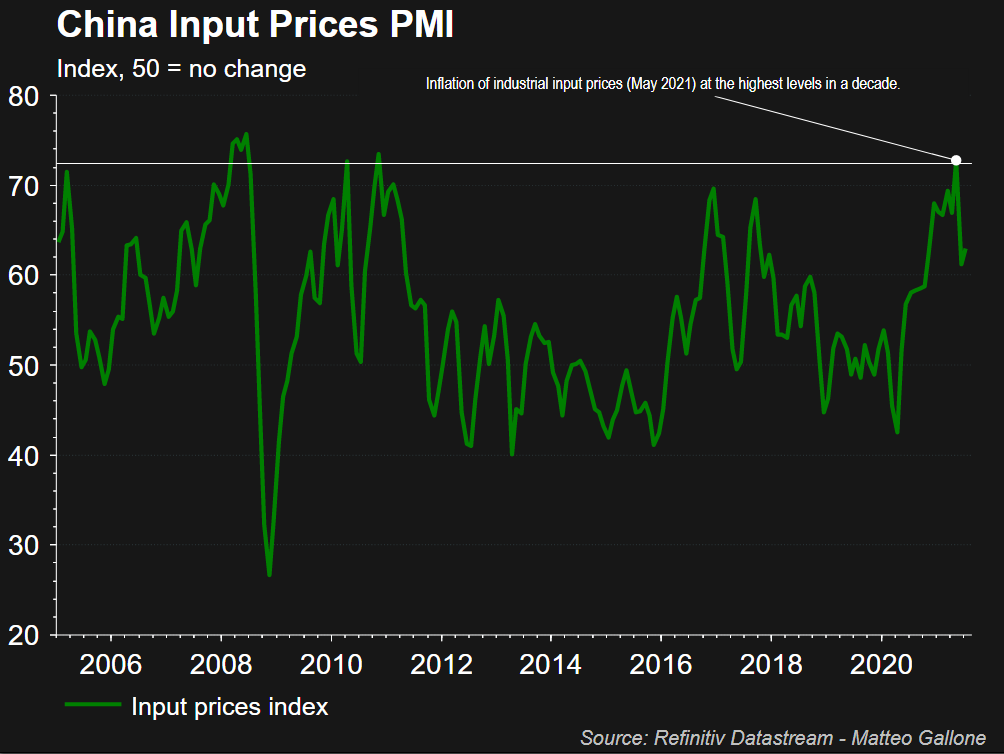

As China's factory prices soared this year, investors feared the country could become a new source of inflation for the rest of the world.

Industrial input price inflation in May 2020 reached its highest level in a decade.

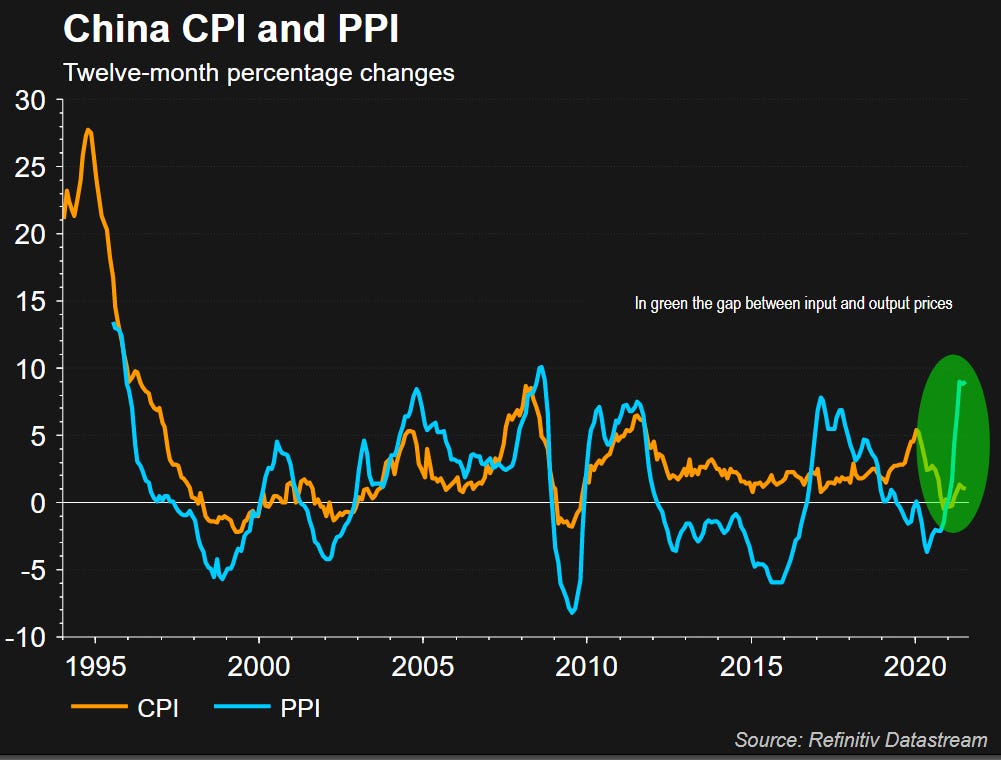

However there is no particular expansion in consumer prices, as a result the gap between China's PPI and CPI has reached a peak since 1990.

There are two alternatives: either companies raise prices, which means higher consumer prices in the medium term, or they can eat the higher input costs and suffer a decline in profits.

But if we widen the field of vision beyond China's borders we will find that China has not contributed to generating global inflation, if anything the world's second-largest economy has helped alleviate some of the price pressures caused by the pandemic and looks like it will continue to do so, at least for a while. Indeed, while some Chinese factories have passed on price increases to Western buyers this year, many are also absorbing higher costs for raw materials such as copper and iron ore themselves.

That has helped keep consumer goods prices from rising even higher elsewhere, though it has also meant lower profits for some Chinese factory owners.

So...not everything is as it seems.

Japan

What are the factors to monitor in the Japanese market?

Japan's core consumer prices reduced their annual pace of decline for three consecutive months in July, a sign that headline commodity inflation was offsetting some of the deflationary pressure caused by a pandemic-induced spending slump. Markets expect consumer inflation to remain well below the levels seen in the U.S. and Europe, as Japan's decision to extend the state of emergency until mid-September appears to deal a blow to already weak household spending.

Cost inflation is driving up commodity prices, while service prices remain weak due to the impact of the pandemic.

Japan's consumer price index, which includes oil but excludes fresh food prices (blue line in the chart below), fell 0.2% in July from a year earlier, marking the 12th consecutive month of decline.

The decline was due in part to a base year change for the CPI that places a greater weight on mobile rates, which fell to a record 39.6% in July.

The so-called core-core consumer price index (green line in the chart below), which strips out not only fresh food but also energy costs, fell 0.6% in July from a year earlier.

These data projections could lead to a cut in the Bank of Japan's inflation forecast at its next quarterly review due in October, as its current projections do not take into account the base-year effect.

Dispassionate advice: keep monitoring.

The Macro Code is an open diary on markets, macro-trends and structural changes.

To receive updates in newsletter format follow the form below.

Please, note that The Macro Code represents personal views only.

Great contents Matteo! About US inflation i would like to observe that there are under the hood not only monetary and "nominal" constrains, like monetary base or whatever, but, moreover, real bottlenecks around the globe, in world trade i mean (see freight fares, sometimes hiked x10 by shipping companies or port closures due to Covid or shortages of raw materials as well) that impede factories to work at full steam. We have, right now, like "physical" constrains that gotta be sorted out and then we could have, probably (i strongly believe), a more "plain-vanilla" way of doing biz around the globe. That should gonna make the economy come back to some normalcy and thereafter, as the economic machine mechanic tells us, make for much moderate inflation rate to which we all are more accustomed to. SB