A Christmas puzzle on global monetary policy

A Christmas puzzle on global monetary policy

A short memo to not get lost in the monetary transition

Welcome to The Macro Code, an open diary on markets, macro-trends and structural changes.

After one month of forced hiatus, the macro newsletter is back.

Introduction

This weekly edition aims to build a macro framework on global monetary policy challenges.

The current macro scenario cannot ignore the evolution of COVID-19 and the new Omicron variant. Indeed, the arrival of Omicron has created destabilization in the markets, generating a more wait-and-see attitude for some central banks.

Currently, the Omicron debate is polarized: I) Most health officials globally sound very cautious, signaling elevated concern about hospital capacity. II) Most market participants are hopeful that the Omicron wave will be milder than previous waves (most Investment Outlooks for 2022 published this month show a constructive attitude about vaccine efficacy towards Omicron). However, the difference in view between health officials vs market participants may not be about simple math (good models vs bad models). It is more a matter of what role each group is playing.

Health officials are in risk management mode (trying to avoid a negative tail risk: hospitals getting over-run). And that generates a certain type of (very cautious) communication.

Market participants have a different role, they are supposed to generate returns, by taking risk.

Hence, the difference in viewpoint/communication may not be about actual difference in central case projection, but more about a difference in the priority around left-tail vs right-tail of distribution.

In between these two counterparts are the politicians: they have to balance the cost of severe health outcomes vs the cost of restrictions (economic, and personal freedom related). That balance will differ by country.

In this context, central banks are looking from the top to try to avoid taking the wrong direction.

How is monetary policy moving globally?

Major central banks have recognized inflation risks and changed their tone to a more restrictive one.

In the U.S., the Fed doubled the pace of tapering and moved up expectations to three in 2022.

In the UK, the Bank of England (BoE) raised deposit rates for the first time since the start of the pandemic.

In Europe, the ECB announced the end of the Pandemic Emergency Purchase Programme (PEPP) in March and a relatively quick tapering of the Asset Purchase Programme (APP) thereafter.

In all three cases, comments on inflation have become more aggressive. The Fed recognizes inflation risks as a major component of the policy after the Consumer Price Index (CPI) approached 7% in November. In the United Kingdom, the Bank of England now expects inflation to reach 6% in February. In Europe, the European Commission acknowledged that inflation risks are increasing. In addition, other advanced economies’ central banks began taking action more recently. New Zealand, Norway, and Iceland have raised rates slightly, the Bank of Canada (BOC) has ended asset purchases, and the Reserve Bank of Australia (RBA) its yield curve control program. As for the rest of the world, at least 20 emerging market central banks had begun raising interest rates a few months ago.

In the next few paragraphs we focus more closely on the FED and ECB.

FED - Hawkish Christmas

The Fed made another hawkish shift at the December meeting and is now catching up to market pricing and consensus among economists, as the economy is in good shape.

CPI headline inflation is running at the highest level in 39 years, inflation expectations have risen (especially short-term), wage growth is stronger and the labour market is quite tight by many measures (as the decline in labour force seems more persistent than what the Fed and many economists believed just a few months ago).

The Fed still believes inflation will come down next year, despite retiring the word “transitory”, but also that the US economy will reach maximum employment.

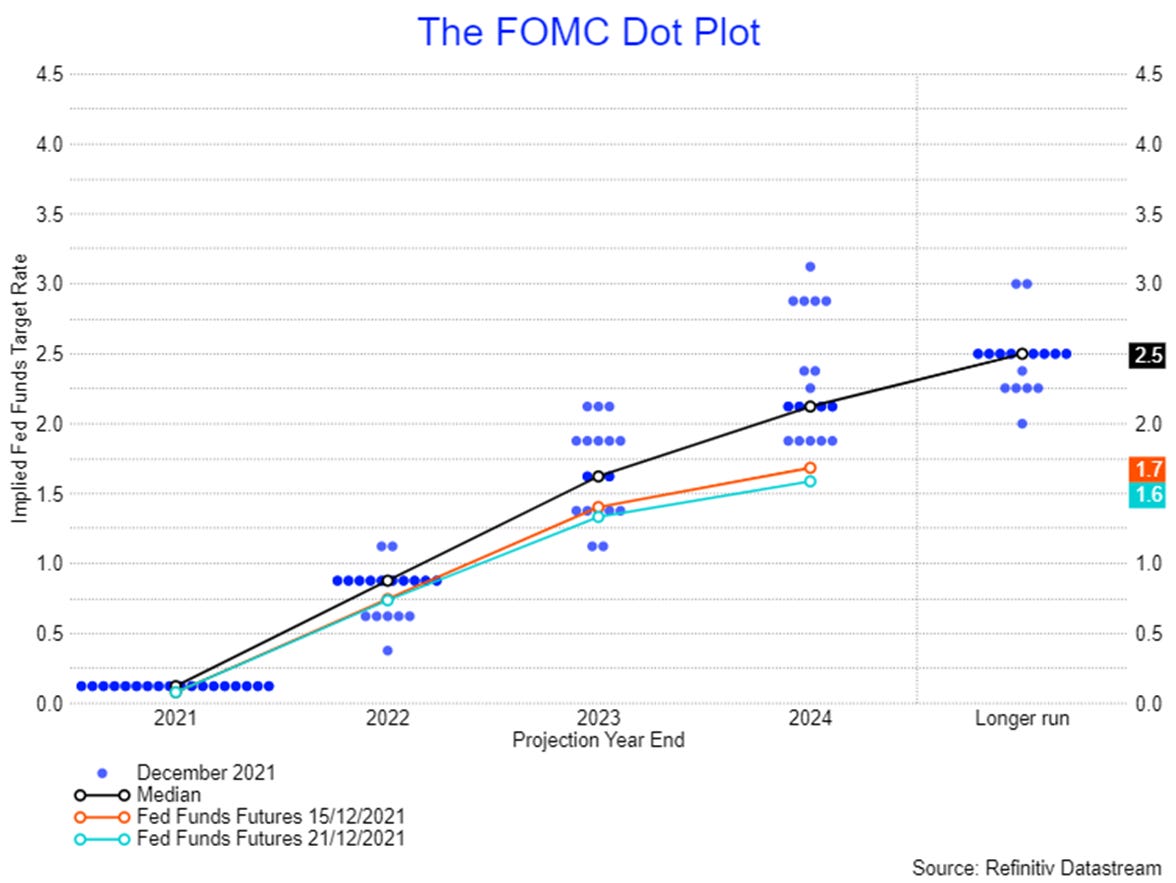

The Fed doubles the tapering pace to USD30bn per month (starting from mid-January), implying QE bond-buying ends in March (from June previously). In addition, the FED's dot plot shows officials expect to raise the fed funds rate three times next year and three times in 2023, based on median projections. The Fed has kept its benchmark rate steady after sweeping into emergency action amid the coronavirus pandemic in March of last year with a full percentage-point cut. Federal Funds Futures, which show where futures markets see the benchmark rate in the future, predict a slightly less hawkish rise.

The hawkish shift was not a surprise given Fed Chair Jerome Powell’s U-turn ahead of the meeting and hence the market reaction was limited.

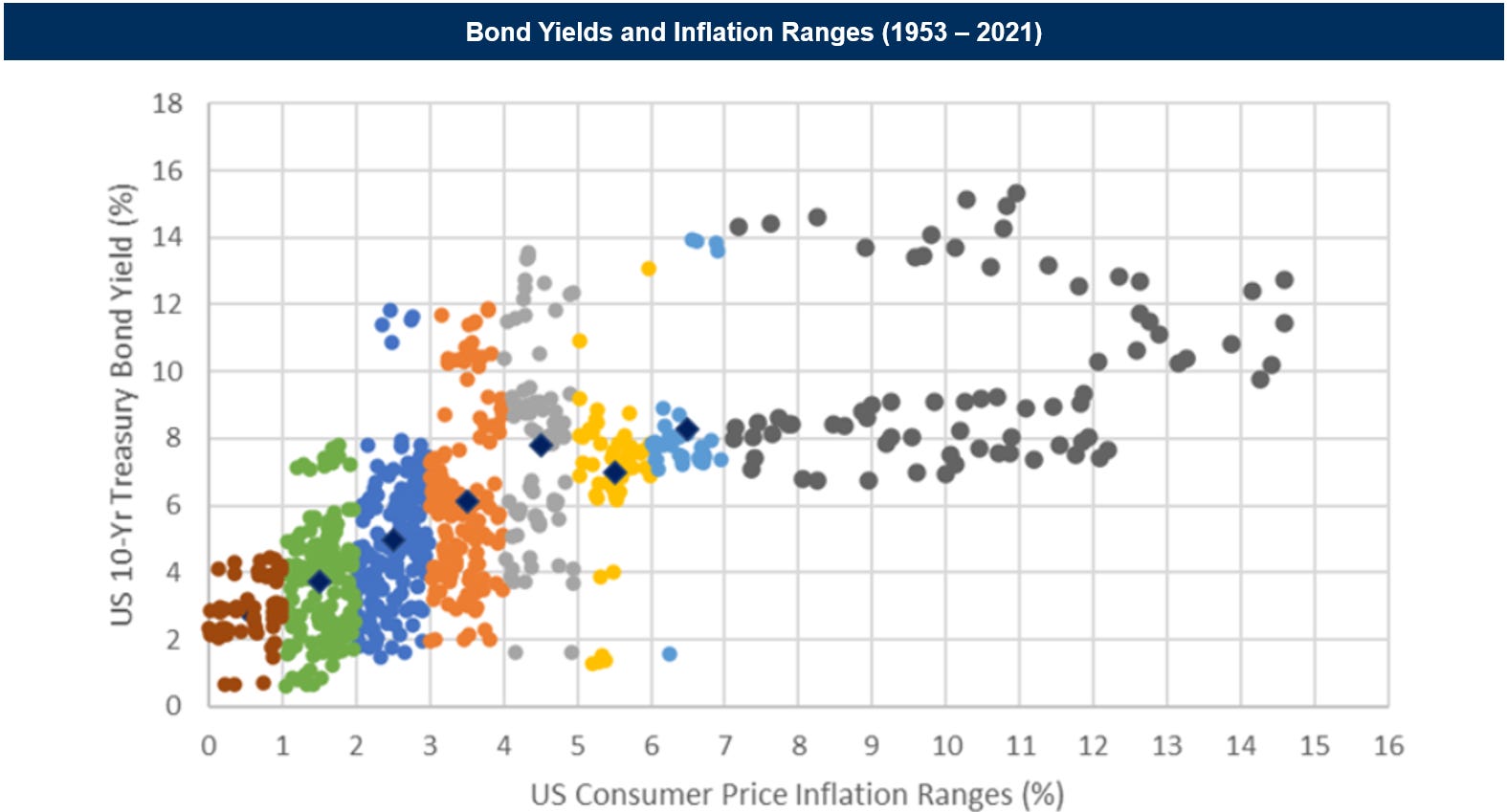

Meanwhile, the U.S. market suffers from no small problem: the gap between inflation and the simultaneous level of bond yields has never been wider.

There are several reasons why bond yields should be higher. The fact that they are not is something to consider in order to weigh whether a portfolio correction is necessary to protect against rising yields and to assess the possible consequences for credit and equity risk premia. For example, the 6.2% increase in consumer prices in October in the U.S. ranks in the 88th percentile of all year-over-year changes since 1953, yet bond yields are only in the 2nd percentile and the effective fed fund rate is even lower.

Based on historical relationships, bond yields should be higher and monetary policy less accommodative. Every time U.S. consumer prices have risen more than 6% in a 12-month period since 1950, yields on 10-year Treasury bonds have been more than 7%.

In the figure below, the blue dot at the lower end of the 6%-7% range is the current level in the United States.

Of course, today's reality is different than in the past, but the fundamental relationship between long-term interest rates and inflation has broken down over the past decade and is now completely misaligned.

ECB - not a matter of wage pressure

The ECB left rates unchanged at historic lows (0 on main refinancing operations, 0.25% on marginal operations, and -0.50% on deposits with the central bank itself) and reiterated that it expects them to remain at or below current levels until it sees inflation reach 2% well before the end of its projection horizon and on a sustained basis for the remainder of the projection horizon. Indeed, it believes that the progress made in underlying inflation is sufficiently advanced to be consistent with a stabilization of inflation at 2 percent over the medium term. This may also imply a transition period in which inflation is moderately above target.

In light of progress on the recovery and on achieving the inflation target over the medium term, the ECB will make a gradual reduction in the pace of securities purchases. In fact, it announced that the pace of purchases under PEPP will be lower in the first quarter of 2022 than in the previous quarter. And it reiterated that it will cease net asset purchases under Pepp, to which it has maintained the total allocation of 1.850 billion euros, at the end of March next year.

But to balance the lack of purchases from the anti-crisis plan, from the second quarter it will double to 40 billion euros per month the purchases made with the App program, ordinary QE, and then continue with 30 billion in the third quarter and return to 20 billion per month from October 2022 for as long as it takes to reinforce the accommodative impact of its official rates.

Not only that. The Governing Council decided to extend the reinvestment horizon for Pepp. It now intends to reinvest principal payments on maturing securities purchased under the Pepp at least until the end of 2024.

With regard to inflation, ECB officials continue to support communication that still reflects a transitory view on inflation in the Eurozone, this is supported by the now well-known trinity of base effects, higher energy prices and bottlenecks. However, increased awareness of the upward risks for inflation has appeared lately. In their communication, the members of the Governing Council made it clear that they would not react to a supply shock, but that the de-anchoring of inflation expectations and the setting of destabilizing wages and prices could turn it into a "bad inflation" (Panetta) which the ECB would need to react to. Although there are no indications of these at the moment, the ECB will be watching wage negotiations in particular very closely.

In addition, Ms. Schnabel - better known as a centrist than a hawk - for example referred not only to closing the output gap but also to structural changes in the global economy when she spoke of upside risks to inflation, for example due to the shortage of skilled labor and the green transition.

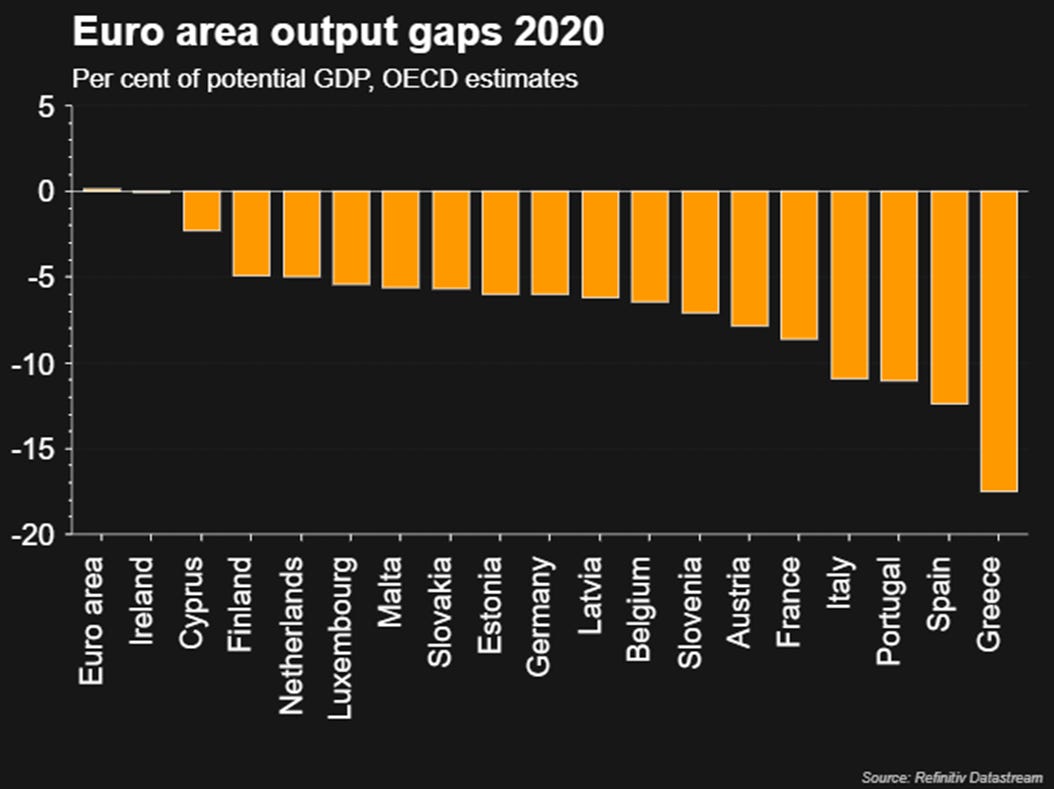

Now future ECB actions are tied to a key question: how much support for the pandemic is still needed given that the disinflationary effect of the pandemic will have largely been eliminated and the output gap will likely be closed in 2022?

The recovery is now largely self-sustaining and there is much less stress and fragmentation than at the start of the pandemic. What the ECB does in the end will depend critically on the Governing Council's view of the development of the pandemic, taking into account a triad with different visions: markets (extreme confidence in vaccinations), health officials (extreme caution on the new variant development), politicians (introduce strict containment measures to avoid overload in hospitals).

In this scenario, the ECB cannot afford to copy the moves of the FED with the usual time lag. This is because the macroeconomic dynamics related to inflation between the Eurozone and the US are different. Europe lost less labor during lockdowns than the US, thanks to leave programs.

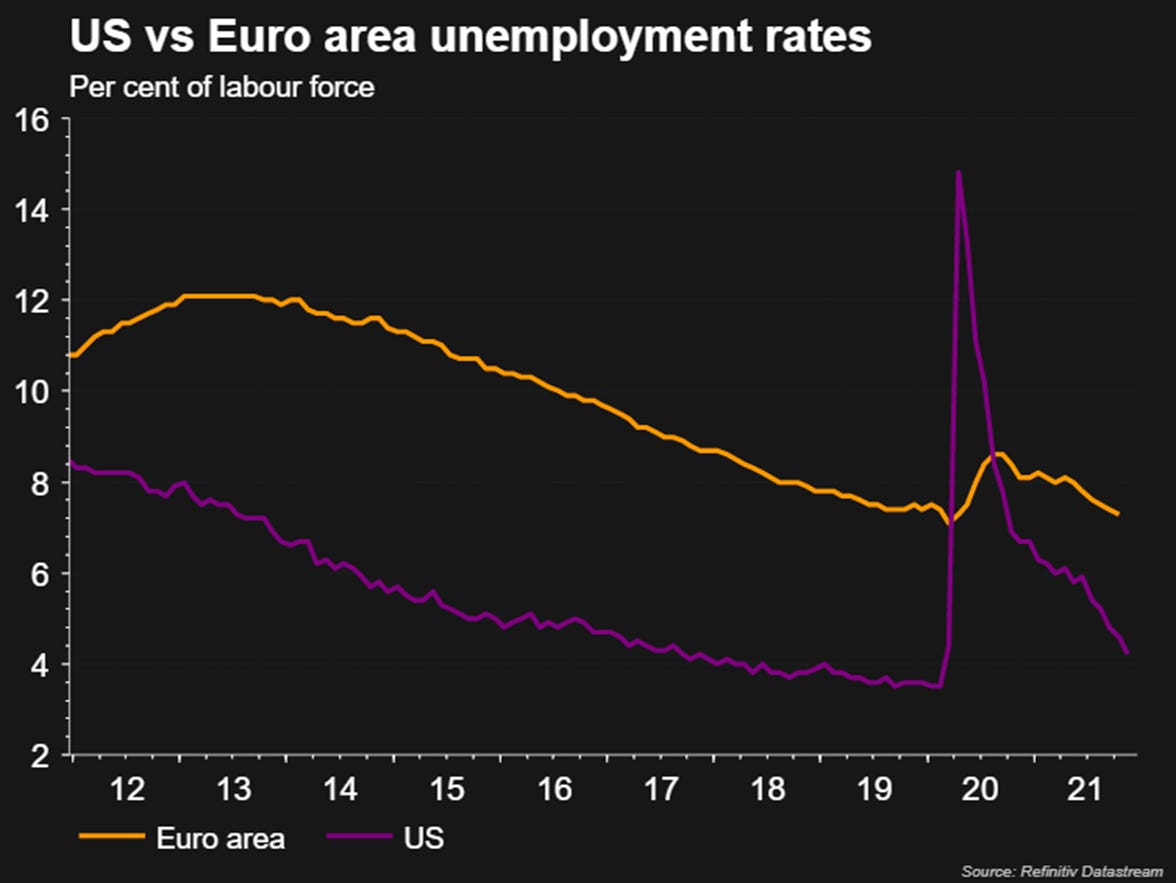

In theory, core inflation depends primarily on how much wages grow relative to productivity. The difference between the two is measured by the growth in unit labor costs, which are now falling in most sectors. This allows European producers to absorb some of the increase in non-labor production costs, a very different situation than in 2007 and 2008 when both wages and rising commodity prices squeezed margins (see figure below). Moreover, the current decline in unit labor costs mirrors their rise in 2020, a pendulum swing that was in sync with the shutdown and then sudden restart of economies. These mechanisms allowed euro area employment to recover quickly and smoothly. Of the 5 million jobs canceled in the spring 2020 freeze, 4.7 million have already been recovered by the third quarter of 2021.

In some countries, e.g., France, employment is already above its pre-pandemic level. The labor force participation rate also appears to have returned to pre-crisis levels in the eurozone, in tune with GDP, while it is still 1.5 percentage points lower in the United States, even with a faster GDP recovery.

This gradual recovery in Europe's labor market is translating into moderate wage growth. Negotiated wages increased by 1.5 percent in 2021, up from 1.9 percent a year earlier. But the rapid recovery in employment also means that Europe is once again approaching the "full employment" situation it was in before COVID-19. The vacancy rate (2.5%) is at an all-time high, and a growing share of companies point to labor shortages as a factor limiting their production. The eurozone unemployment rate is close to its structural level (7.6% in 2021, according to the OECD), warranting an acceleration of negotiated wages toward 2%-2.5%. This seems to be the range of wage increases currently being discussed by the social partners and already agreed upon in Germany for next year. Even if the minimum wage in Germany were to be increased by 25% in 2022, as proposed by the government, it would only benefit about 2% of workers and should be viewed in light of a 1.9% wage increase in 2022 that German unions have already negotiated for about 14% of the country's workers.

However, the pace of wage increases remains below the productivity gains projected for 2022 (3.1%) and not much above the productivity gains projected for 2023 (1.5%). This suggests that wage inflation driven by a price-wage spiral will likely not become apparent in the near term (at least through 2023).

The Macro Code is an open diary on markets, macro-trends and structural changes.

To receive updates in newsletter format, follow the form below.

Please, note that The Macro Code represents personal views only.